|

M

A S I

M A N A G E R I A L R A T I O S

by

H A N S J E S S E N

The Technical University

of Denmark

November 1982

AMT Publication

DI.82.85-A

.

ABSTRACT

In order to determine

managerial ratios as mathematical analytical functions of time there has

been developed a graphical model of a firm. This model shows the physical relationship

between fundamental principles of bookkee- ping, operating statements and

managerial economics. The model is the structural basis of the

determination of the mathematical analytical functions for management.

The analytical

background of traditional ratio techniqu- es, including, Bela Gold lit. 40

and the Dupont pyramid, is described by means of a new developed general

manage-rial ratio funktion.

.

- I -

CONTENTS

Page

Sumary V

Preface VI

Part A:

CHAPTER A

1. An analytical business model 1

1.1. Introduction 1

1.1.1. S. Eilon's model 1

1.1.1.1. Functional relationships and assumptions 3

1.1.1.1.1. Change in the cost structure 7

1.1.1.1.2. Change in the earnings structure 13

1.1.2. Assessment of S. Eilon's

model

18

Part B:

CHAPTER_B

2. An analytical graphical business model 20

2.1. Activity parameters 20

2.1.1. Sales

20

2.1.2. Purchases

20

2.1.3. Inventories 22

2.2. Payment parameters, operations

2.2.1. Sales

22

2.2.2. Purchases

23

2.3. Market parameters, sales 23

2.3.1. Cash sales ratio q 23

2.3.2.

The price p 24

2.3.3. Debit time dD 24

2.4. Market parameters, purchases 25

2.4.l. Cash purchases ratio

e 25

2.4.2. The price q1 of raw materials 26

2.4.3.

The price q2

of labor hours 26

2.4.4 Credit time dK 27

- II -

3.1. Income statement 28

3.1.1.

Sales of goods 28

3.1.2.

Costs 29

3.1.2.1.

Inventories, additions (with signs) 30

3.1.3. Resource consumption (incl. F'i,1) 33

3.1.4.

Operating profit (before interest and deprec.) 33

3.1.5.

Operating profit incl. inventory deprec. 33

4.1. Chanqe in liquidity (operations) 35

5.1. Cash balance 36

5.2. Bank loans 36

5.3. Loans (long-term)

37

6.1. Investment (in fixed capital)

38

7.1. Depreciation (for tax purposes) 39

8.1. Interest (for tax purposes)

40

9.1. Tax pavments 4O

10.1. Principal ratios 41

10.1.1.

Operating profit 0'(t) 41

10.1.2.

Change in liquidity l'(t) 42

10.1.3.

Working capital K(t)

43

10.1.4. Contribution ratio DG(t) 43

10.1.5.

Depreciation 44

10.1.6. Interest r'BL(t) 44

.

- III -

CHAPTER C

11. An analytical mathematical businessmodel 45

11.1. Physical and financial functions i

the operating

system

45

11.1.1. Sales

45

11.1.2. Inventories 46

11.1.3. Output

50

l1.1.4. Sales, ingoing payments 50

11.1.5. Purchases, outgoing payments

51

11.1.6. Change in liquidity 52

11.2. Capital tied up in the operating

system 52

11.2.1. Trade accounts receivable 52

11.2.2. Trade accounts payable 53

11.2.3. Raw materials invefitory 53

11.2.4. Finished goods inventory 54

11.2.5. Working capital (tied up in the operating system

54

12.1. Operatinq profit (for accountinq purposes) 55

12.2. Operating profit (computed on the

basis of Fig. 2.1.) 56

12.2.1. Operating profit incl. inventory depreciation

58

12.3.1. Bank loans

59

12.3.2. Loans (long term) 60

12.3.3.

Investments 60

12.4.1. Interest payments 61

12.4.2. Depreciation 61

12.4.3. Tax payments 61

12.4.4. Cash flow released 62

12.4.4.1.

Interest relative 63

12.4.4.2.

Depreciation relative 63

.

- IV -

13.1. Traditional ratios 64

13.1.1 Contribution ratio 64

13.1.2. Profit ratio 64

13.1.3. Break-even sales 64

13.1.4. Margin of safety 65

13.1.5. Applications, examples 65

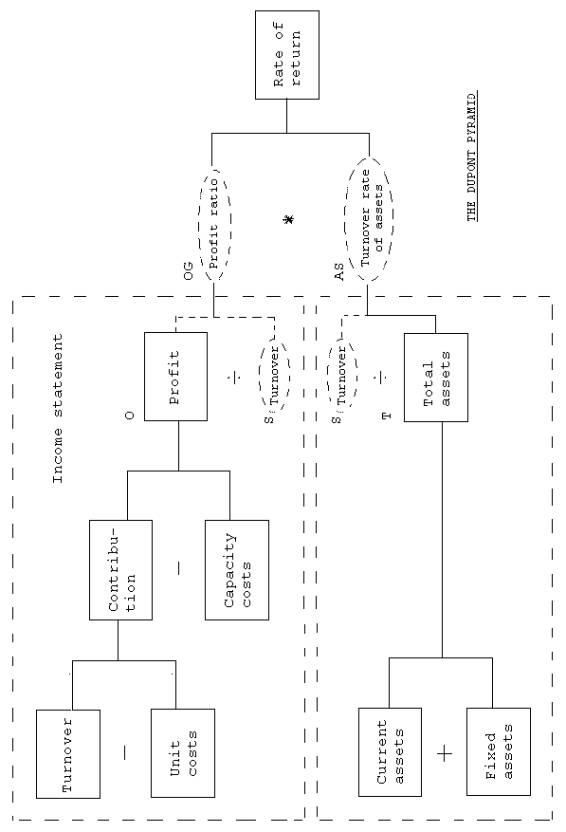

13.2. Dupont pyramid 66

13.2.1 Ratio mathematics, general

68

CONCLUSION 7O

BIBLIOGRAPHY 72

.

- V -

SUMMARY

For the determination of ratios as

analytical mathematical functions of time a graphical model of a firm has been

developed. This model is a graphical representation of the relationships

between fundamental aspects of the firm relating to book-keeping (records),

accounting and managerial economics. The model forms the basis of the

following deve- lopment of analytical mathematical functions. The

mathematical back-ground of traditional ratio techniques, including Bela

Gold lit. 40 and the Dupont pyramid, is shown through the development of a

general ratio function.

Lyngby, November 1982

.

- VI -

PREFACE

The existing literature on accountancy

and managerial economics has ma- de several attempts to improve the

theoretical basis in order to provide management with a better

understanding of business management possibili- ties.

In lit. 20, Albert Danielsson is dealing

solely with purely analytical

aspects in relation to costs of

production, and he has in that connec- tion developed symbolic flow charts

for analysis purposes. This work seems to be of a very special character and

not suited for overall ma- nagement purposes where the firm is to be seen

as a whole. Links to inventories and the market are, for instance, missing.

Bela Gold, lit. 40, attempts to

generalise accounting ratios in a tech-nical structure which includes

managerial ratios. This technique seems to be very practicable but only for

partial global business analyses. In this thesis a theoretical analysis of

general ratios will be made, in-cluding the Dupont pyramid and including,

in particular, Bela Gold's ratio technique.

J. W. Forrester, lit. 37, provides with

his special representation

technique based on computer technology an

excellent basis for analy- sing company behavlour. It gives, in a certain

degree, a good insight into the behavlour of a firm in situations with

different external and internal influences. Also here a fundamental

mathematical model for purely analytical purposes is missing.

Dan Ahlmark, lit. 1, stresses the

necessity of developing an analysis

model of the business which makes it

possible to consider the current

integrated process, production,

investment, financing activities of the business. To illustrate this need,

an extensive empirical business ana- lysis is made, using generally known

simulation techniques.

.

- VII -

Finn C. Sørensen, lit. 97, finds in his

review of traditional accoun-

ting methods that a model should be

developed for man agement which is

suitable for illustrating general matters

in the firm, i.e. form the

basis of an actual managerial audit. By this

is meant an examination of activities and matters underlying the

financial/accounting report.

Samuel Eilon, lit. 30, attempts with his

mathematical model to compute

the rate of return as a function of

general business parameters, using, among other things, a symbolic

graphical representation technique to de-scribe the inter relationships of

the equations. This work seems to be the most interesting work in the

literature seen in relation to the de- velopment of a generalised business

analysis model.

Using the literature reviewed as a

starting point with special impor-

tance being attached to the above

authors, the structure and field of

applications of Eilon's model in lit. 30

will be analysed in detail.

After this analysis, a graphical

analytical business model is developed in Chapter B including book keeping,

accounting and financial concepts to be employed by the business

management. Using this model it is possi-ble to carry out an actual

managerial audit as described by Finn C. Sø- rensen, among others.

Chapter C defines an analytical

mathematical business model based on the general graphical structure shown

in Chapter B. As a special starting point is taken the fact that any sales

curve may be composed of a piece- wise linear function. The basic element

of the sales function is thus chosen as a linear function of time.

Based on the developed mathematical

functions the most common accounting ratios are computed as a function of

time.

.

- VIII -

Bela Gold's ratio technique is examined

more ciosely, using general ma-thematical ratio functions developed in this

report, and an attempt is made to explain it by means of these functions,

which are also used to illustrate

the technical background of the computation of the rate of return in the

Dupont pyramid.

.

C

H A P T E R A

.

- 1 -

1.

An analytical business model

1.1.

Introduction

During the mentioned review of the

litterature only one source was found, which was suitable for forming the

basis of the development of

the general mathematical business model

in Chapters B and C. This sour- ce was Samuel Eilon's article in OMEGA

1997, Vol. 5, No. 6: "A Profita- bility Model for Tactical

Planning", lit. 30.

In the following the mentioned article

will therefore be discussed as

an introduction to the analytical

mathematical business model in Chap-

ter C.

1.1.1

S. Eilon's model

The article starts by pointing out that

simple models reflecting aggre- gate company behaviour in response to

changes imposed by management de- cisions and/or outside factors provide

useful tools for management for tactical planning purposes.

As his starting point, Eilon takes the

rate of return r expressed as:

(p - c)V

r = ¾¾¾¾¾

(1)

I

or

earnings

r =

¾¾¾¾¾¾¾¾¾¾¾ (2)

total investment

where

.

- 2 -

p = unit price per unit of output

c = unit cost per unit of output

V = output units per time unit

I = total investment

Attention is drawn to the fact that for

macro economic purposes it is

possible to compute the ratio r from the

definition equation (2) and

thus obtain information on an industry's

"profitability".

Equation (1) is a micro economic

rewriting of (2) based on "logical"

considerations. The numerator in equation

(1) is fairly well defined,

also in a micro economic model, but the

denominator I, total assets,

which serves the main purpose, is

difficult to determine in practice.

Additions to and disposals of assets as

well as changes in the market

value of these assets take place currently.

The practical purpose of the computation

of the rate of return is a

desire to obtain an equivalent measure of

the return on investment. It

appears from the above that in practice

the com putation of r involves

great uncertainty so that r is a relatively

uncertain measure of profi- tability. If the following definitions are now

introduced

dp dc dI

p* = ¾¾¾ ;

c*

= ¾¾¾ ; I* = ¾¾¾ ,

p d I

where the changes dp, dc, dV and dI are

given, equation (1) can be

transformed into

1 1 + V*

r* = ¾¾¾¾¾¾ (¾¾¾¾¾ (p* - (1 - a) c*) + V* - I*) (3)

1 + I* a

.

- 3 -

p - c

given definition a = ¾¾¾¾¾ = the relative

profit margin.

p

As regards equation (3), S. Eilon

observes that it is an analytical tool for assessing the effects on r of

changes of the variables of the

right hand side.

In practice, a functional inter

relationship exists very often between

these variables; a later change in the

selling price or the cost price will, for instance, bring about changes not

only in investments (in

the working capital) but also in demand

and hence output.

1.1.1.1.

Functional relationships and assumptions

Eilon assigns to the cost c per output

unit the following conventional

functional expression:

F J

c = s + ¾¾ + ¾¾ (4)

V V

where

s represents direct

unit costs

F

¾¾ represents indiret unit costs excl. interest

V

J

¾¾ represents interest

charge per unit.

V

Equation (4) is a so called traditional

economic calculation of total

unit costs. It should, however, be noted

that from a general accoun-

ting point of view there is no real

justification for equation (4). It

is simply an appropriate formula for the

unit cost function in relati-

on to the traditional theory of

managerial economics, which makes it

possible to carry out simple partial

operations research computations

.

- 4 -

concerning, for instance, profit

maximization in relation to various

alter natives.

The stressing of the point that equation

(4) has no real physical ju-

stification is due to the fact that

equation (4) is a simple transfor- mation of equations (5) and (6).

TO = c V (5)

TO = s V + F + J (6)

Equation (5) is here a purely non

physical definition equation (addi-

tion of simple "krone amounts")

for the total costs TO specified via

the definition equation (6). It will be

seen that these definition equa- tions give rise to problems in connection

with the physical interpreta- tion. What is, for instance, meant by fixed

costs, and how are they de- fned in relation to, say, the interest charges

J ?

A transformation of equation (4) using

the definitions s = f1 c , F/V

= f2 c and J/V = f3 c gives

1

c* = f1 s* + ¾¾¾¾¾(f2 F* + f3 J* - (1 - f1) V*) (7)

1 + V*

This equation (7) shows that with a good

approximation we have:

c* = f1 s* + f2 F* + f3 J* - (1 - f1) V* (8)

Interpretation of the contents of, for

example, (8) will show that the

percentage change of the unit costs is

equal to the weighted sum of the percentage change of s, F, J and V.

.

- 5 -

Concerning investments I, S. Eilon

assumes:

IW = A + B (9)

I = IW + IF (10)

where

IW = the working capital

IF = investment in fixed assets

B

= bank loans + overdrafts

A

= other loans

S. Eilon also defines:

w = IW/I (10a)

l = B/IW (10b)

J = j B , where j is the interest rate (lOc)

Equation (10) can now be transformed

into:

I* = w I*W + (1 - w)I*F

(11)

Equation (9) can be transformed into:

I*W = (1 - l) A* + l B* (12)

A combination of equation (12) and

equation (11) will take the form:

I* = w ((1 - l) A* + l B*) + (1 - w) I*F (13)

For use in the actual planning process of

the business, S. Eilon assu-

mes that

.

- 6 -

I*F = 0 (14)

and

A* = 0

(15)

It is also assumed that w and l are constant (the artiticle does not

mention this explicitly).

Based on the mentioned assumptions

equations (12) and (13) are then

reduced to

I*W = l B* (16)

and

I* = w l B* (17)

gives the conditions (14) and (15).

In connection with the determination of

changes in the working capital

IW, S. Eilon writes:

"No single relationship between

working capital and the 1evel of ac-

tivity in the firm is universally

accepted and we may proceed to ex-

plore two possible assumptions."

These two assumptions are combined as a

linear combination

I*W = g (p v)* + h(c V)* (18)

which denotes that the working capital

(tied up in the operating sy-

stem is changed as a linear combination

of the change in sales and the

change in cost. S. Eilon claims that no

controller has difficulty in

determining empirically the constants g

and h. It must therefore be

.

- 7 -

possible to find a physical model which

describes these empirical facts. A mathematical analytical solution to this

problem is described

in Chapter C.

S. Eilon proceeds to consider three cases

which are relevant for tac-

tical planning purposes:

1. Change of s, F and j

2. Change of V

3. Change of p

In the first case changes in the cost

structure are considered. The

following two cases deal with changes in

sales and changes in the mar-

ket price, i.e. two situations where the

earnings structure is chan-

ged. However, as regards cases 2 and 3, it

is natural to describe them

together as will be seen later. The

things to be discussed are therefo- re as follows:

1. Change in the cost structure caused by

changes in s, F and j.

2. Change in the earnings structure

caused by changes in V given the

market elasticity e.

1.1.1.1.1. Change in the cost structure

Attention is drawn to the fact that in

his case 1 S. Eilon discusses

an iterative process, physical and

mathematical, in connection with the final computation of c*. From a physical point of view,

this is in full accordance with the accounting theory, as will be shown

later in the ge- neral mathematical business model. S. Eilon attempts to

provide this "fact" of the expressions de scribed here through the mathematical convergence in the computation

of total unit costs as shown in the article. In this respect, however, it

does not seem to be a good idea to combine physical and mathematical facts

too much since, as has already been

- 8 -

mentioned, S. Eilon employs a non physical

definition of unit costs (see equation (4), which highly weakens the

foundation of Eilon's conclusi- ons.

S. Eilon elaborates on this definiton of

the unit cost, one of the prin- ciples of traditional theories of

managerial economics, in case 1. It is exactly these conflicts between the

physical conditions in the firm and the traditional theory of managerial

economics which have caused the de- velopment of the mathematical business

model described in Chapter C.

With a view to solving the existing

mathematical problem, equation

(1Oc) is transformed into:

J* = j* + (1 + j*) B* (2o)

The mathematical problem can now be

solved by means of the followinq

previously shown equations (7), (16) and

(18) together with the reated conditions:

Equations:

1

c* = f1 s* + ¾¾¾¾ (f2 F* + f3 J* - (1 - f1) V*) (21)

1 + V*

J* = j* + (1 + j*) B*

(22)

I*W = l B* (23)

I*W = g(p v)* + h(c v)* (24)

.

- 9 -

given the conditions

V* = 0

(25)

p* = 0 (26)

A solution is obtained as follows:

From equation (24) with the conditions

(25) and (26) it follows that

I*W = h c* (27)

Equation (27) and (23) give

h

B* = ¾¾

c* (28)

l

A combination of equation (28) and (22)

gives

h

J* = j* + (1 + j*) ¾¾ c* (29)

l

A combination of equation (29) and (21)

gives

f1

s* + f2 F* + f3 j*

c* = ¾¾¾¾¾¾¾¾¾¾¾¾¾¾ (30)

h

1 - (1 + j*) ¾¾ f3

l

In equation (30) the question is raised whether

h

(1 + j*) ¾¾ f3 < 1

l

has been satisfied as, in practice,

equation (lOb) shows that

1 IW

¾¾ = ¾¾

l B

.

- l0 -

Normally will IW < B, hence

1

¾¾ < 1

l

As typically in practice h < 1, f3 < 0.5 and (1 + j*) < 1.5, inequa1ity

(31) gives

h 1

(1 + j*) ¾¾ f3 < 1,2 ¾¾ 0.5

l 1

or

h

(1 + j*) ¾¾ f3 < 0.6

l

From this will be seen that, in practice,

inequality (31) has been sa-

tisfied.

S. Eilon introduces a new ratio H = IW /(c V) for the purpose

showing

that inequality (31) has been satisfied

in practice. This seems to be

a purely mathematical exercise without

any relevant justification phy-

sically. It is once more pointed out that

S. Eilon overinterprets the

mathematical consequences of the use of

the equation (4) defined on the basis of managerial economics.

For the purpose of computing the rate of

return the equations (3),

(lOa) and (18) are used to solve the

equations:

1 1 + V*

r* = ¾¾¾¾¾ (¾¾¾¾¾(p* - (1 - a) c*) + V* - I*) (32)

1 + I* a

1

I =

¾¾ IW (33)

w

.

- 11 -

I*W = g(p V)* + h(c v)* (34)

with the conditions:

f1

s* + f2 F* + f3 j*

c* = ¾¾¾¾¾¾¾¾¾¾¾¾¾¾ (35)

h

1 - (1 + j*) ¾¾ f3

l

V* = 0 (36)

p* = 0

(37)

Equation (34) gives, cf. equation (27)

I*W = h c* (38)

Equation (33) is transformed into

I* = w I*W (39)

Equatioin (38) combined with equation

(39) gives

I* = w h c* (40)

Equation (32) gives with equation (40)

and the conditions (35),

(36) and (37) the following expression

c*

1 - a

r* = - ¾¾¾¾¾¾¾¾ (¾¾¾¾¾ h w ) (41)

1 + w h c* a

given

f1

s* + f2 F* + f3 j*

c* = ¾¾¾¾¾¾¾¾¾¾¾¾¾¾ (30)

h

1 - (1 + j*) ¾¾ f3

l

.

- 12 -

As regards equation (30) it should be

noted that S. Eilon finds it

"justified" to define a

quantity

c*0 = f1 s* + f2 F* + f3 j* (42)

as unit costs, if h = 0, i.e. if no

changes occur in the working ca-

pital with the given conditions V* = O and p* = 0 , cf. equa tion (38).

Equation (35) now takes the form

c*0

c* = ¾¾¾¾¾¾¾¾¾¾¾¾¾¾ (30)

h

1 - (1 + j*) ¾¾ f3

l

given

c*0 = f1 s* + f2 F* + f3 j*

Further, on the basis of the denominator

in equation (43), S. Eilon

defines a ratio u as he seems to find it desirabie

that all ratios oc-

cur in product form. For instance, as

mentioned previously in this

connection, he also defines the ratio H =

IW/(c V), which from the

point of view of accounting theory is a

very specific concept.

A look at equation (43) will show that it

takes the form of "ratios",

i.e. it contains dimensionless

quantities, which are all ratios in the

firm. Therefore, it does not seem to be a

very desirable measure to

introduce further ratios to give the equa tion a changed algebraic

structure.

However, for analytical purposes in

connection with an analysis of the

numerical "behaviour" of

equation (43) it may be useful to define a

parameter x given by

.

- 13 -

h

x =

(1 + j*) ¾¾ f3 (44)

l

so that equation (43) is transformed into

c*0

c* = ¾¾¾¾¾ (45)

1 - x

given

h

x =

(1 + j*) ¾¾ f3 (46)

l

and

c*0 = f1 s* + f2 F* + f3 j* (47)

Thus, by a preliminary nurnerical

analysis of (45), x may be a11owed

to vary in the interval 0 < x < 1.

It should be noted that x is here a

parameter. In the second phase of such an

anal ysis a numerical ana- lysis of

equation (46) can be carried out, given certain selected va- lues of x.

1.1.2.1.2. Change in the earnings structure

In this case where management wishes to

consider the influence of the

market on the rate of return, etc., the

following expression is assu-

med to apply

V* = - e p* (48)

given p*.

.

- 14 -

The problem is thus given by the

equations

1

c* = f1 s* + ¾¾¾¾¾ (f2 F* + f3 J* - (1 - f1) V*) (49)

1 + V*

J* = j* + (1 + j*) l B*

(50)

I*W = l B* (51)

I* = g(p V)* + h(c V)*

(52)

with the conditions:

s* = 0

(53)

F* = 0

(54)

j* = 0 (55)

V* = - e p* (56)

Here equation (52) is transformed into

I*W = (g + h)V* + (g p* + h c*)(1 + V*) (56a)

After the transformation of the above

equations and with the above

conditions the following equations are

developed:

1

c* = ¾¾¾¾¾ (f3 B* - (1 - f1) V*) (57)

1 + V*

1

B* =

¾¾((g + h) V* + (g p* + h c*)(1 + V*)) (58)

l

given the condition V* = - e p* (59)

.

- 15 -

Now equations (57), (58) and (59) give by

simple reduction

e

p*

1 f3

c* = (1 - f1) ¾¾¾¾¾ ¾¾¾¾¾¾¾¾¾¾ (1 - ¾¾¾¾¾¾¾

1 - e

p* f3 (1 - f1) l

1 - ¾¾¾ h

l

(h + g(1 + p* - e-1))) (60)

given the conditions

s* = 0

(61)

F* = 0

(62)

j* = 0 (63)

V* = - e p* (64)

In connection with the practical use of

equation (60) it might be de-

sirable to define a change in the unit

cost cx* given by

e

p*

c*x = (1 - f1) ¾¾¾¾¾¾ (65)

1 - e

p*

which has been obtained by putting s* = 0, F* = 0 and J* = 0 in equati- on (7). c*x can here be interpreted as the

change in the unit cost if the only thing to be considered is a change in

the price p.

Moreover, from equation (60) can be

defined

g

y = ¾¾¾

h

which may be interpreted as the need of

investment in the working ca-

pital caused by sales in relation to

caused by costs (see equation (18)).

.

- 16 -

The system of equations (60) .... (64) is

now given the form

c*x x

c* = ¾¾¾¾ (1 - ¾¾¾¾ (1 + y(1

+ p* - e-1))) (66)

1 - x 1 - f1

given the conditions

h

x =

(1 + j*) ¾¾ f3 (67)

l

g

y = ¾¾¾

h

Using equations (3), (17), (57) and (60)

.... (64) the following sy -

stem of equations can now be defined for

the determination of the rate

of return.

Equation:

1 1 -

e p*

r* = ¾¾¾¾¾¾¾ (¾¾¾¾¾¾ (p* - (1 - a) c*) - e p* - w I*W) (69)

1 + w I*W a

given the conditions

s* = 0 (70)

F* = 0

(71)

j* = 0

(72)

V* = - e p* (73)

I*W = (g + h)V* + (g p* + h c*)(1 + V*) (74)

e

p* 1 f3

c* = (1 - f1) ¾¾¾¾¾ ¾¾¾¾¾¾¾¾¾¾ (1 - ¾¾¾¾¾¾¾

1 - e

p* f3 (1 - f1) l

1 - ¾¾¾ h

l

(h + g(1 + p* - e-1))) (75)

.

- 17 -

If changes are recorded only in V, the

following system of equations

is obtained by replacing p* with V* and putting p* = 0 and e-1 = 0 in

the above equations:

V* 1 f3

c* = - (1 - f1) ¾¾¾¾¾ ¾¾¾¾¾¾¾¾¾¾ (1 - ¾¾¾¾¾¾¾

1 - V* f3 (1 - f1) l

1 - ¾¾¾ h

l

(h + g)) (76)

given the conditions

s* = 0

(77)

F* = 0

(78)

j* = 0 (79)

e-1 = 0

(80)

p* = 0

(81)

and the system of equations:

1 1 - a

r* = ¾¾¾¾¾¾¾ (V* - ¾¾¾¾¾ (1 + V*) c* + w I*W) (82)

1 + w I*W a

given the conditions

s* = 0

(83)

F* = 0 (84)

j* = 0

(85)

I*W = (g + h(1 + c*)) V* + h c* (86)

V* 1 f3

c* = - (1 - f1) ¾¾¾¾¾ ¾¾¾¾¾¾¾¾¾¾ (1 - ¾¾¾¾¾¾¾

1 - V* f3 (1 - f1) l

1 - ¾¾¾ h

l

(h + g)) (87)

Attention is called to the fact that the

resuits in this Chapter dif-

fer from S. Eilon's results in cases 2

and 3. The following Chapter

will indude a general discussion of S.

Eilon's results and models in

the light of the results achieved here.

- 18 -

1.1.2. Assesment of S. Eilon's model

It has already been pointed out that the

basis of S. Eilon's model gi- ves rise to the question as to whether it

serves any purpose to carry out these computations and at the same time

attach such fundamental importance to the models shown in the article in

relation to the phy- sical business situation.

Thus, S. Eilon assumes that eguation

(4) is fundamental, i.e. a funda- mental starting point for

considerations based on managerial economies. With reference to eguations

(5) and (6) it was stated that this is a point of view which should be

examined more closely. This examination leads to the point that eguation

(4) is a purely mathematical definition equation, i.e. an equation which

is not founded on real physical facts (equation (6)'s right hand side

consists of a sum of elements of widely differing physical origin with only

one thing in

common: the value "DKK").

Owing to the mathematical structure of

equation (4) it will mathema-

d J(V)

tically be convergent as where U £ ¾¾¾ (¾¾¾)

£ K , in practice U

dV V

and K are constants. The physical

convergence also exists in connec- tion with the changes in the tactical

planning process (transients) under consideration. It should be noted that

the mathematical model shows the relationships between changes in

states" (i.e. time is not included explicitly) with the related

mathematical characteristics of the manner of converging. The physical

activity/cash flow model of the business is knovn also in practice to

possess convergent characteri- stics as a function of time. See chapter C.

Against this background it is important

not to attach too great impor-

tance here to the applicability of S.

Eilon's model to an interpreta-

tion of the dynamics of the firm (for

tactical planning purposes).

Thus, the mathematical business model,

Chapter C, is not to take state

functions as its starting point but only

use a time description of the

functions.

.

- 19 -

The graphical description used by S.

Eilon can only be regarded as a

dear description of the equations between

the individual variable.

being studied.

In Chapter B a physical model description

of the business will the-

refore be given first, the greatest

importance being attached to ma-

king the physical/financial description

as realistic as possible. Af-

ter this the mathematical déscription is

developed in Chapter C.

The results achieved in the present

Chapter A differ from S. Eilon's

results as far as computations of the

effects of changes in the ear-

nings structure are concerned. It is

pointed out that S. Eilon's un-

structuralized consideration of the

mathematical methods of solution

may be the reason for the deviating

results in the article.

The central equation (18), which

estimates the relationship between the working capital tied up in the

operating system, will be analysed in detail in Chapter C.

.

C H A P T E R

B

.

- 20 -

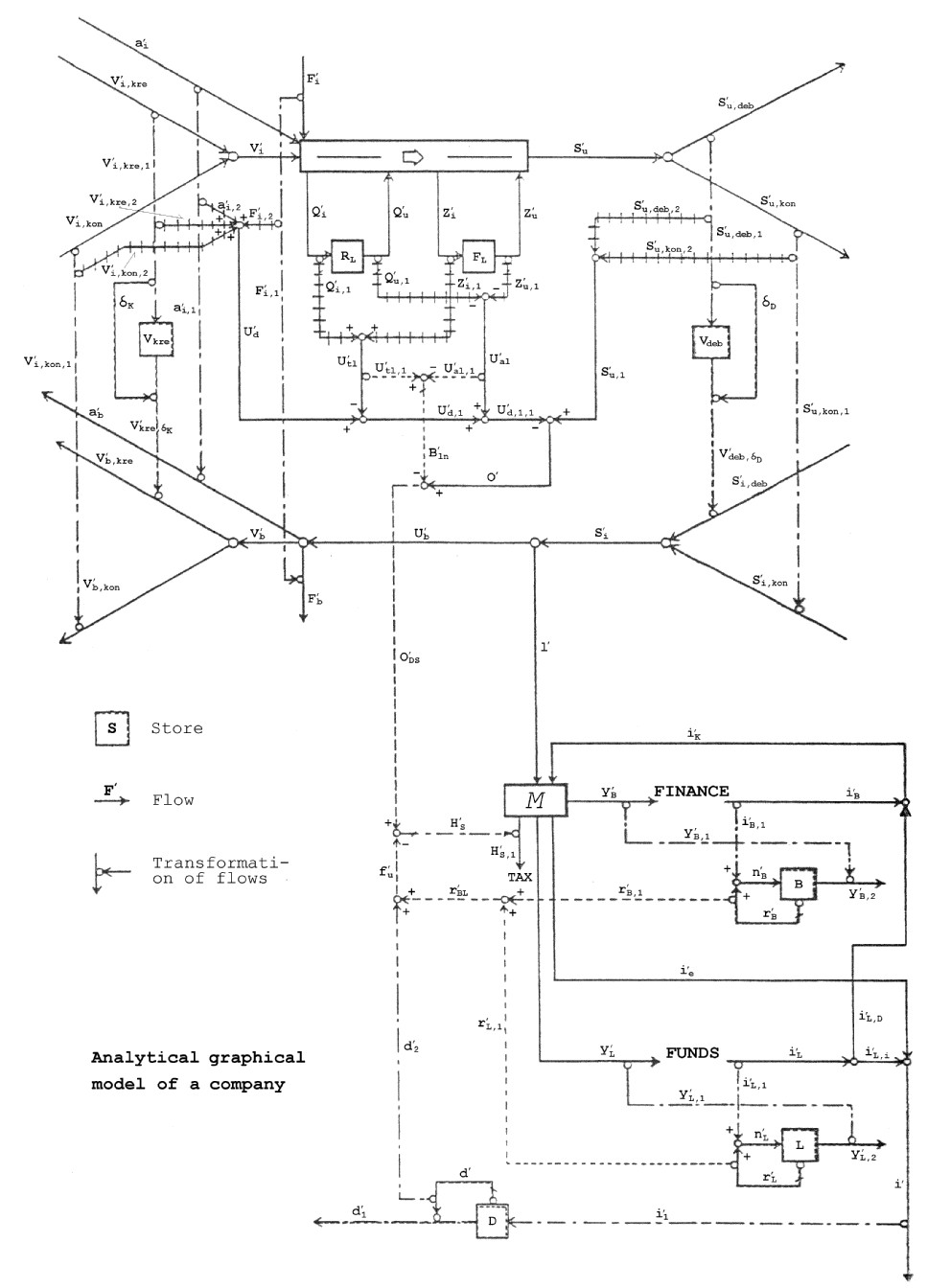

2.

An analytical graphical business model

This Chapter describes an analytical

graphical business model (see Fig. 2.1.). This model will form the basis of

a mathematical analytical description of the business so that this

description can be used by the business management for their principal

planning activities. The model will integrate principal elements of

managerial economics and the ac- counting theory, it being assumed that the

business comprises an acti- vity/cash flow and related principal assets

(accounts payable, accounts receivable, inventories). It is management's

task to achieve the best possible composition of this general structure by

using some of the ra- tios defined in the model.

2.1. Activity

parameters

2.1.1. Sales

The volume of goods sold by the firm per

unit is denoted with S'u. Sales are here divided into

two main components of which one is the reference sales S'u,kon, which refers to the share of

sales which is paid for in cash. The other component of sales is denoted

with S'u,deb,which refers to the share of

sales which is paid for by the trade accounts receivable the debit time

deltaD

after delivery

from the firm. Here the following eguation applies:

S'u(t) = S'u,deb(t) + S'u,kon(t)

(88)

2.1.2.

Purchases

The firm is supplied with a number of

labor hours per time unit a'i.

The firm is supplied with the volume of

goods per time unit V'i. This flow of goods consists

of two main components of which one is the refe- rence purchase V'i,kon, and the other the goods

purchased on credit V'i,kre, which are paid for by the

firm after the credit time dK.

- 21 -

Figure

2.1

(Click

on the figure for 200%)

.

- 22 -

The following equation applies:

V'i(t) = V'i,kre(t) + V'i,kon(t)

(89)

The firm is supplied with the fixed

volume of resources per time unit F'i. This flow of resources may,

for example, include electricity, administration, heating, rent, etc.

2.1.3.

Inventories

The

volume of raw materials per time unit Q'i is added to the raw mate-

rials inventory consisting of the volume

RL. From the raw materials in-

ventory is deduced the raw materials volume Q'u. The following equation

applies here:

t

RL = ò (Q'i(t) - Q'u(t))dt (90)

0

The

volume of finished goods per time unit Z'i is added to the finished

goods

inventory consisting of the volume FL. From the finished goods

inventory is deduced the finished goods

volume Z'u. The following equa- tion applies here:

t

FL = ò(Z'i(t) - Z'u(t))dt

(91)

0

2.2. Payment parameters, operations

2.2.1. Sales

The total volume of means of payment per

time unit from the customers is denoted with S'i. This payments flow consists of

two components. One component is the payments flow S'i,kon stemming from the cash sales

flow

S'u,kon. The other component S'i,deb is the payments flow stemming

from the credit sales flow S'u,deb. Here the following equation

applies:

S'i(t) = S'i,kon(t) + S'i,deb(t)

(92)

.

- 23 -

2.2.2. Purchases

The total volume of means of payment per

time unit for operations is denoted with U'b. This payments flow is

composed of three components, a'b and V'b and F'b. a'b is the payments flow

corresponding to the flow of hours consumed a'i, V'b is the payments flow

corresponding to the flow of raw material purchases V'i, F'b is the payments flow

corresponding to the flow of fixed resources consumed F'i. The following equation

applies:

U'b(t) = a'b(t) + V'b(t) + F'b(t) (93)

The payments flow V'b is made up of two components.

One component is the payments flow V'b,kon corresponding to the cash

purchases of rawmaterials V'i,kon; the other component is the

payments flow V'b,kre corresponding to the credit

purchase of raw materials V'i,kre. The following equation

applies:

V'b(t) = V'b,kon(t) + V'b,kre(t)

(94)

2.3.

Market parameters, sales

With a viev to depicting the fundamental

financial effects of the mar- ket on the firm as well as its effects on

earnings the market is cha- racterized by three basic components q , p and dD. They also describe the

fundamental link between the firm's sales of goods and the related payments

flows.

2.3.1.

Cash sales ratio q

The cash sales ratio is defined by the

equation;

S'u,kon(t) = q S'u(t) (95)

where 0 £ q £

1

In a manufacturing business q will typically be placed in the in-

terval 0 £ q

£ 0.2.

In a supermarket q will typically be in the interval 0.8 £ q £ 1.

.

- 24 -

2.3.2.

The price p

The price of the firm's product(s) is

defined by the eguations

S'u,kon,1(t) = p S'u,kon(t) (96)

S'i,kon(t) = S'u,kon,1(t)

(97)

where S'u,kon,1(t) is the flow of debts

corresponding to the sales flow S'u,kon(t) (i.e. the current sending

out of invoices stating the amount of debt; see equation (96)). Equation

(97) expresses the fact that the flow of debts S'u,kon,1(t) is equal to the payments

flow from the customers (cash payment).

In practice, it should be noted that

there is normally only a tempora- ry time lag between invoicing and sales.

However, it has a temporary negative effect on liquidity and the

computation of results. Manage- ment will therefore as far as possible make

sure that invoicing is done without the mentioned delays.

2.3.3.

Debit time dD

This model defines the debit time dD as the time from the time of

de- livery of the goods from the firm until the time of payment by the cu-

stomer for the goods. In practice, dD is spread over the individual cu- stomers but with well defined

terms of payment the mean value can be adopted.

The definition of dD can be expressed by the

equations

S'u,deb,1(t) = p S'u,deb(t)

(98)

V'deb,dD(t) = S'u,deb,1(t - dD) (99)

S'i,deb(t) = V'deb,dD(t) (100)

.

- 25 -

S'u,deb,1 refers here to the invoice

flow corresponding to the credit sales flow S'u,deb cf. equation (98). Equation (99)

gives a funational description of a function V'deb,dD(t), which can be defined as

the pay- ments flow (documents) corresponding to the actual receipt of

payments S'i,deb(t) cf. equation (100). In practice, no

time lag is found between the two last mentioned functions.

In pratice, attention should be paid to

the fact that there may be a time lag in the business between invoicing and

sales, the result being changes in liquidity and the computation of

earnings. Management usu- ally aims at applying equation (98) in practice,

i.e. no time lag.

2.4. Market parameters, purchases

With a view to depicting the fundamental

financial effects of the pur- chasing market on the firm as well as its

effects on costs, it is cha- racterized by four basic components epsilon, q1, q2 and dK. They describe the

fundamental link between the firm's purchases of resources and the related

payments flows.

2.4.1.

Cash purchases ratio e

The cash purchases ratio is defined by

the equation:

V'i,kon(t) = e V'i(t) (101)

where 0 £ e £

1

In, say, a manufacturing business e will typically be placed in the interval

0 £ e £ 0.2.

This is also a typical feature in a trading firm.

2.4.2.

The price q1 of raw materials

The price of the firms raw materials is

defined by the equation:

.

- 26 -

V'i,kon,1(t) = q1 V'i,kon(t) (102)

V'b,kon(t) = V'i,kon,1(t)

(103)

where V'i,kon,1(t) is the flow of debts

corresponding to the raw materials flow V'i,kon(t) (i.e. the current receipt

of invoices stating the amounts of debts); see equation (102). Equation

(103) expresses the fact that the flow of debts V'i,kon,1(t) is equal to the payments

flow to suppliers (cash payment).

In practice, attention should bepaid to

the fact that the time lag between the supplier's invoicing and the

supplies of raw materials is usually a temporary feature which has a

temporary positive affect on liquidity and the computation of results.

2.4.3. The price q2 of labor hours

The price of the firm's labor hours is

defined by the equations

a'i,1(t) = q2 a'i(t) (104)

a'b(t) = a'i,1(t) (105)

where a'i,1(t) is the time ticket flow

corresponding to the flow of labor hours used a'i(t) (i.e. the current issuing

of time tickets stating wages earned); see equation (17). Equation (18)

expresses the fact that the time ticket flow a'i,1(t) is equal to the time rate

flow a'b(t).

In practice there is a certain time lag

between functions on the right hand side and the left hand side of the

equal sign in equation (104). This time lag is ignored here. There is

usually no time lag between

the functions of equation (105), or the

time lag is relatively small and of no importance here.

.

- 27 -

2.4.4. Credit time dK

This model defines the credit time dK as the time from the time of de-

livery of the raw materials to the firm until the time of payment by the

firm for the raw materials. In practice, dK is spread over the in-

dividual suppliers but with well defined terms of payment the mean va- lue

can be used. The definition of dK can be expressed by the equati- ons:

V'i,kre,1(t) = q1 V'i,kre(t) (106)

V'kre,dK(t) = V'i,kre,1(t - dK)

(107)

V'b,kre(t) = V'kre,dK(t) (108)

where V'i,kre,1(t) refers here to the invoice

flow corresponding to the

credit purchases flow V'i,kre(t), cf. equation (106).

Equation (107) gi-ves a functional description of a function V'kre,dK(t) which can be defined as

the payment order flow (documents) corresponding to the actual effecting of

payments V'b,kre(t), cf. equation (108). In practice,

there is no time lag between the two last mentioned functions.

In practice, attention should be paid to

the fact that the time lag between the supplier's invoicing and the

supplies of raw materials is usually a temporary feature which has a

temporary positive affect on liquidity and the computation of results.

The following equations are defined in

relation to the fixed resources consumed F'i and the related fixed costs F'b.

F'i,1(t) = k F'i(t)

(109)

F'b(t) = F'i,1(t)

(110)

.

- 28 -

where F'i,1(t) in equation (109) refers to

the flow of debts in the form of invoices (stating amounts) corresponding

to the fixed resoures flow F'i(t). k denotes a symbolic operator in the form

of an average price of the fixed resources unit. In practice, there is some

time lag between the functions in eguation (110). As, however, the fixed

costs by definition are constant in time, such a time lag is not important

in this context.

3.1 Income statement

In this Chapter an income statement for

operations is presented (be- fore depreciation, etc.) using the general

main principles of accoun- ting theory.

3.1.1 Sales of goods

Sales of goods are defined on the basis

of the following equations:

S'u,kon,2(t) = S'u,kon,1(t)

(111)

S'u,deb,2(t) = S'u,deb,1(t)

(112)

S'u,1(t) = S'u,kon,2(t) + S'u,deb,2(t) (113)

Eguation (111) expresses the fact that

the flow of debts (in the form of invoices with statement of amounts) S'u,kon,1(t) gives rise to an e- qually

large information flow S'u,kon,2(t). This quantity is

identital with the current crediting to the cash sales account.

From equation (112) follows that the flow

of debts S'u,deb,1(t) causes an equally large information

flow S'u,deb,2(t). This quantity is iden-

tical to the current crediting to the credit sales account.

Total uales in the form of the

information flow S'u,1(t) corresponding to the total

crediting to the sales account are then obtained from e- quation (113).

.

- 29 -

3.1.2

Costs

The costs of the firm in connection with

production and sales are de- fined by the following equations:

V'i,kon,2(t) = V'i,kon,1(t)

(114)

V'i,kre,2(t) = V'i,kre,1(t) (115)

a'i,2(t) = a'i,1(t)

(116)

F'i,2(t) = F'i,1(t)

(117)

U'd(t) = V'i,kon,2(t) + V'i,kre,2(t) + a'i,2(t) + F'i,2(t) (118)

Equation (114) expresses the fact that

the invoice flow from the cash purchase V'i,kon,1(t) is corrently debited to

the cash purchases account

to

the extent of the cash flow V'i,kon,2(t).

Equation (115) expresses the fact that

the invoice flow from the cre- dit purchase V'i,kon,1(t) is currently debited to

credit purchases account to the extent of the cash flow V'i,kre,2(t).

Equation (116) denotes the functional

relationship between the time ticket flow a'i,1(t) and the current debiting to

the time rate account of the wage payment flow a'i,2(t).

Equation (117) expresses the functional

relationship between the in- voice flow F'i,1(t) for fixed costs and the

current debiting of the cash flow F'i,2(t) to the fixed costs

account.

The total cost flow is defined by

equation (118).

.

- 30 -

3.1.2.1

Inventories, additions (with signs)

By way of introduction, it is mentioned

that the signs relating to additions to inventories (as a mean time value)

are assumed to be the same as those relating to additions to sales (as a

mean time value). Against this background the additions to the individual

inventories will for principal planning purposes have the same signs. The

inventories only serve as "standby stores" in case of emergancy events"

i.e. in normal operation state "the materials and products go directly

through the factory. Thus, the following systems of equations apply:

Q'i(t) > 0

Q'u(t) = 0

d S'u

¾¾¾¾ > 0 Þ (119)

dt

Z'i(t) > 0

Z'u(t) = 0

Q'i(t) = 0

Q'u(t) = 0

d S'u

¾¾¾¾ = 0 Þ (120)

dt

Z'i(t) = 0

Z'u(t) = 0

Q'i(t) = 0

Q'u(t) > 0

d S'u

¾¾¾¾ < 0 Þ (121)

dt

Z'i(t) = 0

Z'u(t) > 0

.

- 31 -

The system of equations (119) denotes

that inventories rise when sales rise.

The system of equations (120) denotes that

inventories are constant when sales remain unchanqed.

The system of equations (121) denotes

that inventories fall when sales fall.

Based on these main principles for the

model the following equations can be developed.

Q'i,1(t) = qR Q'i(t) (122)

Q'u,1(t) = qR Q'u(t) (123)

Z'i,1(t) = qF Q'i(t) (124)

Z'u,1(t) = qF Z'u(t) (125)

U'tl(t) = Q'i,1(t) + Z'i,l(t)

(126)

U'al(t) = Q'u,1(t) + Z'u,1(t)

(127)

where

Q'i,1(t)

is the flow of additions to raw materials invento-

ries corresponding to the additions to

rawmateri-

als inventory records with statement of

amounts.

Q'u,1(t)

is the flow of deductions to raw materials invento-

ries corresponding to the deductions to raw

mate-

rials inventory records with statement of

amounts.

Z'i,1(t)

is the flow of additions to finished goods invento-

ries corresponding to the additions to

finished

goods inventory records with statement of

amounts.

.

- 32 -

Z'u,1(t)

is the flow of deductions to finished goods inven-

inventories corresponding to the deductions

to fi-

nished goods inventory records with

statement of

amounts.

qR denotes the caiculated rav material price

per unit

of finished goods.

qF denotes the caiculated direct cost

price per unit

of finished goods.

U'tl(t)

is total additions to inventories.

U'al(t)

is total deductions from inventories.

The system of equations (119), (120) and

(121) can nov be given the form:

d S'u

¾¾¾¾

> 0 Þ U'tl(t) > 0

and U'al(t) = 0 (128)

d t

d S'u

¾¾¾¾

= 0 Þ U'tl(t) = 0

and U'al(t) = 0 (129)

d t

d S'u

¾¾¾¾

< 0 Þ U'tl(t) = 0

and U'al(t) > 0 (130)

d t

Attention is dravn to the fact that the

physical model based on the FIFO principle can be deseribed mathematically

only by

d S'u

sign ( ¾¾¾¾ ) = sign (U'tl(t)) (131)

d t

given U'al(t) = 0 (132)

and U'tl(t) is computed with signs.

.

- 33 -

3.1.3.

Resourceconsumption (incl. F'i,1)

Resources consumed U'd,1,1(t) can be defined by the

following equations:

d S'u

¾¾¾¾

> 0 Þ U'd,1,1(t) = U'd(t) - U'tl(t)

(133)

d t given U'al(t) = 0

d S'u

¾¾¾¾

= 0 Þ U'd,1,1(t) = U'd(t) (134)

d t

d S'u

¾¾¾¾

< 0 Þ U'd,1,1(t) = U'd(t) - U'al(t)

(135)

d t

given U'tl(t) = 0

3.1.4.

Operation profit (before interest and depreciation)

The operating profit (before interest and

depreciation etc.) is defi- ned by the equation:

O'(t) = S'u,1(t) - U'd,1,1(t) (136)

3.1.5

Operating profit incl. inventory depreciation

If a tax year of the length T is

considered in a period of time

t1 £ t £

t1 + T where t1 is a time selected at random,

the following

functions can be defined:

t1+T

Vkøb = ò q1 V'i(t) dt

(137)

t1

w = w(t1) (138)

an = an(t) (139)

In equation (137) Vkøb represents the purchases of goods

in the period t1 £ t £ t1 + T.

Equation (138) defines w(t1) as the total inventory value

at time t1.

an(t) in the equation defines

the inventory depreciation rate.

.

- 34 -

Materials consumed computed for tax

purposes is then derived from the following equation (140):

Vskat = Vkøb + w(t1) - (w(t1)/(1 - an(t1))

t1+T

+ ò (U'tl(t) - U'al(t)) dt) (1 - an(t1 - T)) (140)

t1

For principal planning purposes the mean

time value of an(t) for a given business will

be a constant an and limited i.e.

0 < an < 0.3 . Based on this

assumption equation (140) gives

t1+T

Vskat = Vkøb - (1 - an) ò (U'tl(t) - U'al(t)) dt (141)

t1

Materials consumed for operations is

defined by the following equation

(54a):

t1+T

Vdrift = Vkøb + w(t1) - (w(t1) + ò (U'tl(t) - U'al(t)) dt) (141a)

t1

or

t1+T

Vdrift = Vkøb - ò (U'tl(t) - U'al(t)) dt) (142)

t1

If equation (142) and equation (141) are

combined, the following equations are developed:

t1+T

Vskat = Vdrift + an ò (U'tl(t) - U'al(t)) dt (143)

t1

t1+T

Vskat = Vdrift + ò an(U'tl(t) - U'al(t)) dt (144)

t1

.

- 35 -

On the basis of equation (144) the

following functions can be defined:

U'tl,1(t) = U'tl(t) (145)

U'al,1(t) = U'al(t)

(146)

In equation (145) U'tl,1(t) denotes total additions to

inventories from a taxation point of view. U'al,1(t) denotes in equation (146)

total de-ductions from inventories from a taxation point of view.

With the following definition equation:

B'ln(t) = an (U'tl,1(t) - U'al,1(t)) (147)

equation (144) can be transformed into

t1+T

Vskat = Vdrift + ò B'ln(t) dt

(148)

t1

On the basis of equation (148) the

following equation (149) can be defined:

O'DS = O' - B'ln (149)

where O'DS is the operating profit

adjusted for inventory depreciation.

4.1. Change in liquidity (operations)

The cash flow released by operations, the

change in liquidity, is de- fined by the following equation (150):

l'(t) = S'i(t) - U'b(t) (150)

.

- 36 -

5.1. Cash balance

The cash balance of the firm is

designated by M, which, in relation to the present principal planning

model, is very small in practice, i.e. M(t) = 0. The following equation can

now be developed:

i'e = l' + i'K - y'B - y'L - H'S,1 (152)

where

i'e is the self financing flow

y'B is the service of bank loans

y'L is the service of other loans

i'K is current raise of loans for operations

H'S,1 is tax payments

5.2. Bank loans

The firm is financed currently by trading

credits in the form of the cash flow i'B. The equation is defined as

follows:

i'B,1(t) = i'B(t)

(152)

where i'B,1(t) is the information flow in

the form of loan documents with statement of amounts corresponding to the

cash flov i'B(t). The bank charges currently interest r'B(t) on the amount outstanding

B = B(t) where r'B(t) is the document flow with

statement of interest. The following equation appliess:

n'B(t) = i'B,1 + r'B

(153)

where n'B(t) is the firm's current

crediting to the bank account.

.

- 37 -

The current service payments y'B(t) to the bank give rise to a

payment order flow with statement of amounts y'B,1(t). We have:

y'B,1(t) = y'B(t) (154)

The payRent order flov y'B,1(t) involves a corresponding current

debi- ting to the bank account in the form of y'B,2(t). The following equati- on

therefore applies:

y'B,2(t) = y'B,1(t)

(155)

5.3. Loans (long term)

The long term financing of the business is

represented by the cash flow i'L. The following equation

applies:

i'L,1(t) = i'L(t)

(156)

where i'L,1(t) is the information flow in

the form of loan documents with statement of amounts corresponding to the

cash flow i'L(t). On the loan L current interest r'L(t) is charged where r'L(t) is the document flow with

statement of interest. The following equation applies:

n'L(t) = i'L,1(t) + r'L(t)

(157)

where n'L(t) is the firm's total

current crediting to the loan account.

The following equation applies:

i'L(t) = i'L,1(t) + i'D(t)

(158)

where i'L,D(t) denotes the long term

financing flow to the working ca- pital, and i'L,1(t) is the long term financing

flow to the fixed capi- tal.

.

- 38 -

The following equation applies:

i'K(t) = i'B(t) + i'L,D(t) (159)

The current service payments y'L(t) to lender give rise to a payment

order flow with statement of amounts y'L,1(t). We have

y'L,1(t) = y'B(t) (160)

The payment order flow y'L,1(t) involves a corresponding

current debi-ting to the loan account in the form of y'L,2(t). The following equati- on

therefore applies:

y'L,2(t) = y'L,1(t)

(161)

6.1. Investment

(in fixed capital)

The firm's current investment in fixed

capital is denoted i'(t). The following equation applies:

i'(t) = i'L,1(t) + i'e(t) (162)

It is pointed out that, in practice, i'L,D(t) currently converts short

term liabilities into long term liabilities, which means that at a

strategic level alone i'L,D = 0. As to i'e(t), there is no unique defi-

nition of i'e(t) as it depends on the financing and market situation.

Roughly speaking, i'e(t) is the average cash flow

which can be with- drawn from the business without changing the existing

product, invest- nent and financing structure and the necessary financial

reserves set aside for an appropriate future development of the businees.

.

- 39 -

7.1. Depreciation (for tax purposes)

It is normal to distinguish between

depreciation for tax purposes and depreciation for accounting purposes.

Depreciation for accounting pur- poses is used with the object of comparing

alternative projects on the basis of special cost principles, which, for

example, are mentioned in connection with equation (4). These principles

are pure- ly OR mathe- matical models and do not reflect the physical

business situation.

Here we shall only take an overall view

of the financial flow of the firm for which reason depreciation for tax

purposes will be used. Such depreciation will only reflect the actual

effects on liquidity (after tax).

The following equations apply:

i'1(t) = i'(t) (163)

t

D(t) = ò (i'1(t) - d'1(t))dt (164)

0

where i'1(t) represents the current

debiting to the tax depreciation account corresponding to the investment

flow i'(t). d'1(t) is the cur- rent crediting

to the same account (i.e. current "depreciation").

D(t) represents the balance of the tax

depreciation account. The de- preciation charges d'(t) are calculated on the

basis of this account, and the following expressions apply:

d'1(t) = d'(t) (163a)

d'2(t) = d'(t) (164a)

where d'2(t) is the depreciation flow

which is inciuded in the basis of computation of the taxable income.

.

- 40 -

8.1.

Interest (for tax puroses)

Interest is usually computed for two main

purposes. One concerns the income statement for tax purposes, the other

concerns internal compu- tation purposes such as the effect of interest on

the income statement as a whole or in connection with special computations.

No distinction will be made here between

the two purposes. The inter- est charges will be placed in this model with

the sole aim of depic- ting the fundamental financial characteristics.

The following equations are defined:

r'B,1(t) = r'B(t)

(165)

r'L,1(t) = r'L(t)

(166)

r'BL(t) = r'B,1(t) + r'L,1(t)

(167)

where r'B,1(t) denotes the current

recording of interest payment to the

bank. r'L,1(t) denotes the current

recording of interest payments to other lenders. The recording of total

interest payments is designated r'BL(t).

9.1.

Tax payments

According to the principles governing

computation of the taxable income the following equations apply:

f'u(t) = d'2(t) + r'BL(t)

(168)

H'S(t) = s (O'DS(t) - f'u(t))

(169)

H'S,1(t) = H'S(t)

(169a)

.

- 41 -

where f'u(t) is a state function for

the computation of tax, cf. equa- tion (168), s is the tax rate, H'S(t) is the computed tax

payment and H'S,1(t) is the tax payment flow.

10.1. Principal ratios

As appears from Fig. 2.1, the following

principal ratios in the firm are important to the understanding of the

dynamic (tactical) characte- ristics of the firm.

Operating

profit O'(t)

Change

in liquidity l'(t)

Working

capital (net) K'(t)

Contribution

ratio DG(t)

Depreciation

d'2(t)

Interest r'BL(t)

These ratios will be discussed in detail

in the following.

10.1.1. Operating profit O'(t)

Using different assumptions concerning

prices and changes in principal assets (accounts payable, accounts

receivable, inventories) it is pos- sible via Fig. 2.1 to assess the

effects on the operating profit. A reduction of the raw materials

inventories in a situation with raw ma- terials prices which are higher

than the prices of the raw materials inventories but othervise constant

will increase the profit temporari- ly in the period concerned.

One of the things that will be seen is

that the profit O'(t) is inde- pendent of the volume of trade accounts payable

and the volume of tra- de accounts receivable.

- 42 -

10.1.2.

Change in liquidity l'(t)

Other things being equal, the following

expression, cf. Fig. 2.1., ap- plies:

d S'u

¾¾¾¾ > 0 Þ l'(t) < O'(t) (170)

d t

Equation (170) shows that the profit O'(t) is larger than the change

in

liquidity in the case of growing sales in

the firm, the reason being the funds tied up, calculated with signs, in principal

assets (ac-

counts receivable and inventories),

d S'u

¾¾¾¾

= 0 Þ l'(t) = O'(t) (171)

d t

Equation (171) shows that the change in

liquidity is equal to the pro-fit in the case of constant sales, the reason

being an unchanged volu- me of principal assets (accounts payable, accounts

receivable and in- ventories).

d S'u

¾¾¾¾

< 0 Þ l'(t) > O'(t) (172)

d t

From equation (172) appears that in the case

of falling sales the change in liquidity becomes greater than the operating

profit owing to a reduced volume of principal assets (accounts payable,

accounts receivable and inventories).

The above shows how important it is for

the business to keep the cash budget currently up to date as the profit and

the financial circum- stances of the business may differ substantially from

each other. It should be noted that if the net principal assets are

negative, the inequality signs in (170) and (172) must be reversed.

.

- 43 -

10.1.3.

Working capital K(t).

If the working capital is denoted K(t),

the definition eguation for net capital tied up in the operating system

will apply:

K(t) = Vdeb(t) + FL(t) + RL(t) - Vkre(t) (173)

The following definition equation will

also apply:

d K(t)

¾¾¾¾

+ l'(t) = O'(t) (174)

d t

Equation (174) shows that the profit is

equal to the change in liqui- dity + the increment of the net working capital

tied up.

If equation (174) is transformed, the

following equation is derived:

d K(t)

¾¾¾¾

= O'(t) - l'(t) (175)

d t

Equation (175) denotes that the

difference between the operating pro- fit and the change in liquidity is

equal to the financing requirements for operations in the period under

review.

10.1.4.

Contribution ratio DG(t)

The contribution ratio is defined by

equation (176):

DG(t) = (O'(t) + F'b(t))/S'u,1(t) (176)

Equation (176) shows that DG is

independent of the amount of sales and defines the share of sales which

will cover fixed costs, etc. The point is stressed here that a high

contribution ratio does not imply that there is "money" to cover

the fixed costs. For further details see section 10.1.2. as the size of l'(t) gives only an indication

of the ability of the firm to pay fixed costs, etc.

.

- 44 -

10.1.5. Depreciation

Depreciation contributes to influencing the

firm's liquidity, cf. e- quation (169). Assuming that the investments are

made as individual projects at time intervals, it is shown that

depreciation in the peri- ods between investments causes liquidity to rise

owing to the reducti- on in tax payments.

However, it should be noted that of the

cash flow released after tax there must be funds to cover repayment

commitments in connection with loans raised. The effect of the cash flow

released after tax described above is therefore partial and must be seen in

relation to the repay- ment commitments.

In chapter C will be shown that for

practical reasons the division described here is desirable for the

understanding of the financial components of the cash flow released.

10.1.6.

Interest r'BL

From Fig. 2.1 and from equations (168)

and (169) is apparent that in- terest payments reduce the cash flow

released after tax. Thus, the net effect on cash flow released (to be defined in

charter C) stems partly from the computation of income for tax purposes,

partly from the pay- ment of interest on total loans.

The computation of interest on total

loans seen in relation to a given level of activity will be defined later.

.

C H A P T E R

C

.

- 45 -

11.

An analytical mathematical business model

This Chapter presents a new analytical

mathematical model description of the business. This model has been

developed for use in the tactical planning process. No reference can be

made to a similar model in exist- ing literature. The theoretical

literature which gets nearest is S. Eilon's article discussed in Chapter A

in the thesis.

11.1.

Physical and financial functions in the operating system

In the following further definitions of

mathematical functions and their relationships will be established. The

sole justification of these defi- nitions is that they provide the basis of

a clear and generally coherent system of equations between ratios.

11.1.1.

Sales

A basic sales volume is defined:

S'u0 = S'u(0) (177)

where S'u0 is the volume of sales S'u at time t = 0, i.e. at the

beginning of the simulation period.

The development of sales during the time

period is defined by equation (91):

d S'u(t)

¾¾¾¾ = as S'u0 (178)

d t

where as is constant.

.

- 46 -

The following equation now applies:

S'u(t) = S'u0(1 + as t) (179)

where t ³ 0

11.1.2.

Inventories.

Let a ratio hF be defined so that equation

(180) applies:

hF = FL(t)/S'u(t)

(180)

for t ³ 0, hF being a positive constant

which is designated "finished goods inventory time". Another ratio

hR is defined so that equation

(181) applies:

hR = RL(t)/S'u(t)

(181)

for t ³ 0 being a positive constant which is designated "raw

materi- als inventory time".

From equation (180) follows:

FL(t) = hF S'u(t)

(182)

The definition equation applies:

t

FL(t) = FF(0) + ò Z'i(t) dt (183)

0

which substituted into equation (182) gives:

.

- 47 -

t

FL(0) + ò Z'i(t) dt = hF S'u(t) (184)

0

or

t

ò Z'i(t) dt = hF S'u(t) - FL(0) (185)

0

If equation (179) is used in equation (185),

the following expression is derived:

t

ò Z'i(t) dt = hF S'u0 as t + (hF S'u0 - FL(0)) (186)

0

For t = 0 equation (180) gives the

following expression:

hF = FL(0)/S'u(0) (187)

Using equation (187) together with

equation (186) we have:

t

ò Z'i(t) dt = hF S'u0 as t (188)

0

The solution to the integral equation

(188) is:

Z'i(t) = hF S'u0 as (189)

The flow of goods Z'i(t) to the finished goods

inventory may then be defined by equations (190) and (191):

Z'i(t) = hF S'u0 as (190)

for as ³ 0

and

Z'u(t) = - hF S'u0 as (191)

for as < 0

.

- 48 -

Mathematically the physical equations

(190) and (197) may be described by equation (192) for all values of as, i.e.

Z'i(t) = hF S'u0 as (192)

for

- ¥ < as < ¥

With equation (192) the physical

inventory system has been converted to a mathematical model where Z'i(t) can change sign and where

Z'u(t)

= 0 for all t, cf. equation (189).

From equation (181) follows:

RL(t) = hR S'u(t) (193)

The definition equation applies:

t

RL(t) = RL(0) + ò Q'i(t) dt (194)

0

which combined with equation (193) gives:

t

RL(0) + ò Q'i(t) dt = hR S'u(t) (195)

0

or

t

ò Q'i(t) dt = hR S'u(t) - RL(0) (196)

0

If equation (179) is used in equation

(196), the following equation is

derived:

t

ò Q'i(t) dt = hR S'u0 as t + (hR S'u0 - RL(0)) (197)

0

For t = 0 equation (181) gives:

.

- 49 -

hR = RL(0)/S'u(0) (198)

Using equation (197) together with

equation (198) we have:

t

ò Q'i(t) dt = hR S'u0 as t (199)

0

The solution to the integral equation

(199) is:

Q'i(t) = hR S'u0 as

(200)

The flow of goods Q'i(t) to the raw materials inventory

can now be de- fined by equations (201) and (202):

Q'i(t) = hR S'u0 as

(201)

for as ³ 0

Q'u(t) = - hR S'u0 as (202)

for as < 0

Mathematically the physically equations

(201) and (202) can be descri-

bed by equation (203) for all values of as, i.e.

Q'i(t) = hR S'u0 as

(203)

for

- ¥ < as < ¥

With equation (203) the physical

inventory system has been converted to a mathematica1 model where Q'i(t) can change sign and where

Q'u(t) = 0 for all t.

.

- 50 -

11.1.3.

Output

Total output T'p(t) is given by:

T'p(t) = S'u(t) + Z'i(t) (204)

If the ratio ba is here defined as the number

of labor hours used per unit of output and the ratio bR as the raw materials

consumption per unit of finished goods, the equations, resource balance

equations, will apply:

a'i(t) = ba T'p(t) (205)

V'i(t) = bR T'p(t) + Q'i(t) bR

(206)

If equation (204) and equation (206) are

combined, the following equa- tion is obtained:

V'i(t) = bR S'u(t) + bR Z'i(t) + Q'i(t) bR (207)

If equations (179), (192) and (203) are

substituted into equation (207), the following equation is obtained:

V'i(t) = bR S'u0 (1 + (hF + hR + t) as) (208)

Using equations (204), (179) and (192),

equation (205) gives:

a'i(t) = ba S'u0 (1 + as(t + hF)) (208a)

11.1.4. Sales, ingoing payments

Using equations (95), (96) and (97) we

obtain payments derived from cash sales:

S'i,kon'(t) = p q S'u0 (1 + as t) (209)

.

- 51 -

Using equations (88), (95), (98), (99)

and (100) we obtain payments derived from debit sales:

S'i,deb(t) = p (1 - q) S'u0 (1 + as(t - dD)) (210)

Equations (88), (209) and (210) give:

S'i(t) = p q S'u0 (1 + as t) + p (1 - q) S'u0

(1 + as(t - dD)) (211)

or

S'i(t) = p S'u0 (1 + as(t - dD(1 - q))) (212)

11.1.5.

Purchases, outgoing payments

The outgoing payments flow corresponding

to cash purchases of raw ma- terials is expressed by means of equations

(101), (102), (103) and (208) as

V'b,kon(t) = q1 e bR S'u0 (1 + (hF + hR + t)as) (213)

Credit purchases of raw materials cause

an outgoing payments flow which by means of equations (94) (101), (106),

(107) and (108) is computed at:

V'b(t) = e q1 V'i(t) + (1 - e)q1 V'i (t - dK) (214)

Equation (214) is transformed by means of

equation (208) into:

V'b(t) = e q1 bR S'u0(1 + (hF + hR + t) as) +

(1 - e)q1 bR S'u0(1 + (hF + hR + t - dK)as) (215)

Equation (215) is reduced to:

V'b(t) = q1 bR S'u0(1 + as(hF + hR + t - dK (1 - e))) (216)

.

- 52 -

The total payments flow to purchases of

resources is then obtained by using equations (93), (104), (105) and (216):

U'b(t) = q2 a'i(t) + q1 bR S'u0(1 + as (hF + hR + t - dK

(1 - e))) + F'b(t) (217)

By substituting equation (208a) into

equation (217) the total outgoing payments flow is then given by:

U'b(t) = S'u0(q2 ba (1 + as (t + hF)) + q1 bR(1 + as

(hF + hR + t - dK(1 - e))) + F'b(t) (218)

11.1.6.

Change in liquidity

The accounting concept, change in

liquidity l'(t),

here also called cash flow, can then by the use of equations (150), (212)

and (218) be given the following form:

l'(t) = S'u0(p(1 + as(t - dD(1 - q)))

- q2 ba (1 + as(t + hF)) - q1 bR(1 + as

(hF + hR + t - dK(1 - e)))) - F'b(t) (219)

11.2.

Capital tied up in the operating system

Depending on the firm's level of activity

capital will be tied up in the operating system. Capital will be tied up in

trade accounts payable, raw materials inventories and finished goods

inventories as well as accounts receivable (the amounts are indicated with

signs).

11.2.1. Trade accounts receivable

The volume of trade accounts receivable

is defined by the following equation, equations (88), (95), (98) and (99)

being used:

dD

Vdeb(t) = ò p(1 - q)S'u(t - x) dx (220)

0

.

- 53 -

In this model it is assumed that equation

(179) applies. From this equation combined with (220) follows:

dD

Vdeb(t) = p(1 - q) S'u0 ò (1 - as(t - x))

dx (221)

0

The computation of the integral in

equation (221) allows equation (221) to be reduced to:

Vdeb(t) = p(1 - q) S'u0 dD (1 + as(t - 0.5 dD)) (222)

11.2.2.

Trade accounts payable

The volume of trade accounts payable is

defined by the following equation, equations (89), (101), (106) and (107)

being used:

dK

Vkre(t) = ò q1 bR(1 - e) V'i(t - x)) dx (223)

0

Assuming that sales satisfy equation

(179) and that equation (208) applies, equation (223) develops the

following expression:

dK

Vkre(t) = q1 bR(1 - e) S'u0 ò (1 + as(hF + hR + t - x)) dx (224)

0

By computing the integral in equation

(224) this equation is reduced to:

Vkre(t) = q1 bR(1 - e) S'u0 dK (1 + as(hF + hR + t - 0.5 dK)) (225)

l1.2.3

Raw materials inventory

The volume of the raw materials inventory

is given by equation (193). The value of the raw materials inventory RL,1(t) satisfies the equation:

RL,1(t) = q1 bR RL(t)

(226)

.

- 54 -

If equations (193) and (179) are

substituted into equation (226), we have:

RL,1(t) = q1 bR hR S'u0(1 + as t) (227)

11.2.4.

Finished goods inventory

The volume of the finished goods

inventory is given by equation (182). The calculated consumption of

materials and labor hours per unit of finished goods is given by qF, cf. equation (124). The

definition equa- tion applies:

qF = bR q1 + ba q2 (228)

The value of the finished goods inventory

FL,1(t) satisfies the equati- on:

FL,1(t) = qF FL(t) (229)

If equations (182), (179) and (228) are

substituted into equation (229), the following expression is obtained:

FL,1(t) = (bR q1 + ba q2) hF S'u0(1 + as t) (230)

11.2.5.

Working capital (tied up in the operating system)

The total capital tied up in the

operating system, i.e. the working capital K(t), is through the use of

equations (222), (225), (227) and (230) given by:

K(t) = Vdeb(t) - Vkre(t) + RL,1(t) + FL,1(t) (231)

or by substituting into the relevant

places

K(t) = p(1 - q)S'u0 dD (1 + as(t - 0.5 dD))

- q1 bR (1 + e)S'u0 dK (1 + as(hF + hR + t - 0.5 dK))

+ q1 bR hR S'u0(1 + as t)

+ (bR q1 + ba q2) hF S'u0(1 + as t)

or

.

- 55 -

K(t) = S'u0(1 + as t)(hF (bR q1 + ba q2) + q1 bR hR)

+ p(1 - q) dD S'u0(1 + as(t - 0.5 dD))

- q1

bR (1 - e) dK S'u0(1 + as(hF + hR + t - 0.5 dK)) (232)

12.1.

Operating profit (for accounting purposes)

In the following, functions are

established for the computation of operating profit based on accounting

theory.

The turnover of the firm is obtained by

using equations (96), (98), (111), (112) and (113) and is expressed as:

S'u,1(t) = p S'u(t)

(233)

Using equation (233) equation (179)

gives:

S'u,1(t) = p S'u0(1 + as t) (234)

Raw materials consumed corresponding to

sales S'u(t) are given by the equation:

V'for(t) = q1 bR S'u(t)

(235)

or by using equation (179):

V'for(t) = q1 bR S'u0(1 + as t) (236)

The wages paid, time rates, corresponding

to sales S'u(t) are given by the equation:

a'for(t) = q2 ba S'u(t)

(237)

or by using equation (179)

a'for(t) = q2 ba S'u0(1 + as t) (238)

.

- 56 -

By using equations (234), (236) and (238)

the operating profit O'(t) can now be given the form:

O'(t) = S'u,1(t) - V'for(t) - a'for(t) - F'b(t) (239)

or

O'(t) = S'u0(1 + as t)(p - (q1 bR + q2 ba)) - F'b (240)

12.2.

Operating profit (computed on the basis of Fig. 1.1)

In this section the operation profit will

as an alternative be compu- ted directly on the basis of Fig. 2.1.

The costs U'd(t) in connection with sales S'u(t) are given by equation

(118). If equations (89), (102), (104), (106), (109), (110), (114), (115),

(116), (117), (208) and (208a) are substituted into equation (118), the

following equation is developed:

U'd(t) = q1 bR S'u0(1 + (hF + hR + t) as)

+ q2

ba S'u0(1 + (hF + t)as) + F'b (241)

Computed with a plus or minus sign

(positive for inventory) the fol- lowing value is added to the raw materials

inventory, cf. equation (35):

Q'i,1(t) = q1 bR Q'i(t)

(242)

or equation (203) may be used:

Q'i,1(t) = q1 bR hR S'u0 as (243)

Here the definition equation for cost

prices of raw materials per unit of finished goods has been used:

.

- 57 -

qR = q1 bR (244)

The following value is added to the

finished goods inventory, cf. equa- tion (124):

Z'i,1(t) = qF Z'i(t) (245)

or equation (189) may be used:

Z'i,1(t) = (q1 bR + q2 ba) hF S'u0 as (246)

The total value flow to inventories now amounts

to, cf. equations (131) and (132):

U'tl(t) = q1 bR hR S'u0 as + (q1 bR + q2 ba) hF S'u0 as (247)

or by reduction

U'tl(t) = S'u0 as(q1 bR hR + (q1 bR + q2 ba) hF) (248)

The total operating profit is obtained by

using equations (234), (241) and (248) and is expressed as:

O'(t) = S'u(t) - (U'd(t) - U'tl)) (249)