|

M

A S I The response of a linear sales

curve imposed to a micro

economical model of a company Hans Jessen Management Simulator M A S I , P.O. Box 171, DK-2630 Taastrup and Department of Mathematical Modelling The Technical

University of Denmark, DK-2800 Lyngby,

Denmark (November 11, 1998) Abstract A model of a company based on common accounting

practice for tactical planning is developed containing physical flow of materials,

manhours and deposits of materials, value flow and deposits of value and

financial flow and deposits as functions of time. In the first place a

graphical model is described naming each part by a mathematical function.

Thereafter the functions of time are determined with respect to accountancy

and their solutions are found imposing a linear sales curve. These solutions

describe fundamental functions in time of basic theory of accountancy with

reference to the flow of resources. E.g. profit and loss account, cash flow,

working capital and main key figures of the Dupont Pyramide are determined as

functions of time. Key words:

Flow of resources, accountancy, cash flow, working

capital, key figures, Dupont Pyramide. 1. INTRODUCTION This

paper is concerned with a model of a company containing common accoun- ting

practice. Such models have been presented by Bela Gold,7 with a keynumber technique, which were based on a

very simple ratio technique. Jay W. Forre- ster,6 developed models based on signal-graph - 2 - techniques,

but these models of system dynamics are difficult to apply in practice

because of the data to be found and to be interpreted. Models more applicable

for management analysis and decisions were developed by Albert Danielsson,2-3 in the form of flow-graphs but containing no

mathematical func- tions for evaluation. Samuel Eilon,4-5 made some mathematical approach to describe the

primary problem of this article, the equations as functions of time between

the working capital and the working system of profit and loss account,

without also considering the derived cash flow. His model as well as others

on this very aggregated data level are not able simultaneously to measure

values from the basic theory of accountancy as functions of time. In the litterature of accountancy

and management e.g. C. J. Malmborg,8

Alfred Rappaport,9 and R.S.

Segal,10 one will find no functions of time describing and

being consistent with accounting practice. Among

all these efforts to describe the processes of products and finance in a

company one will find Dan Ahlmark,1 as a primary source for this study. Dan Ahlmark only

made a general desciption without mathematical modelling of ac- countancy

with functions of time. - 3 – 2. An

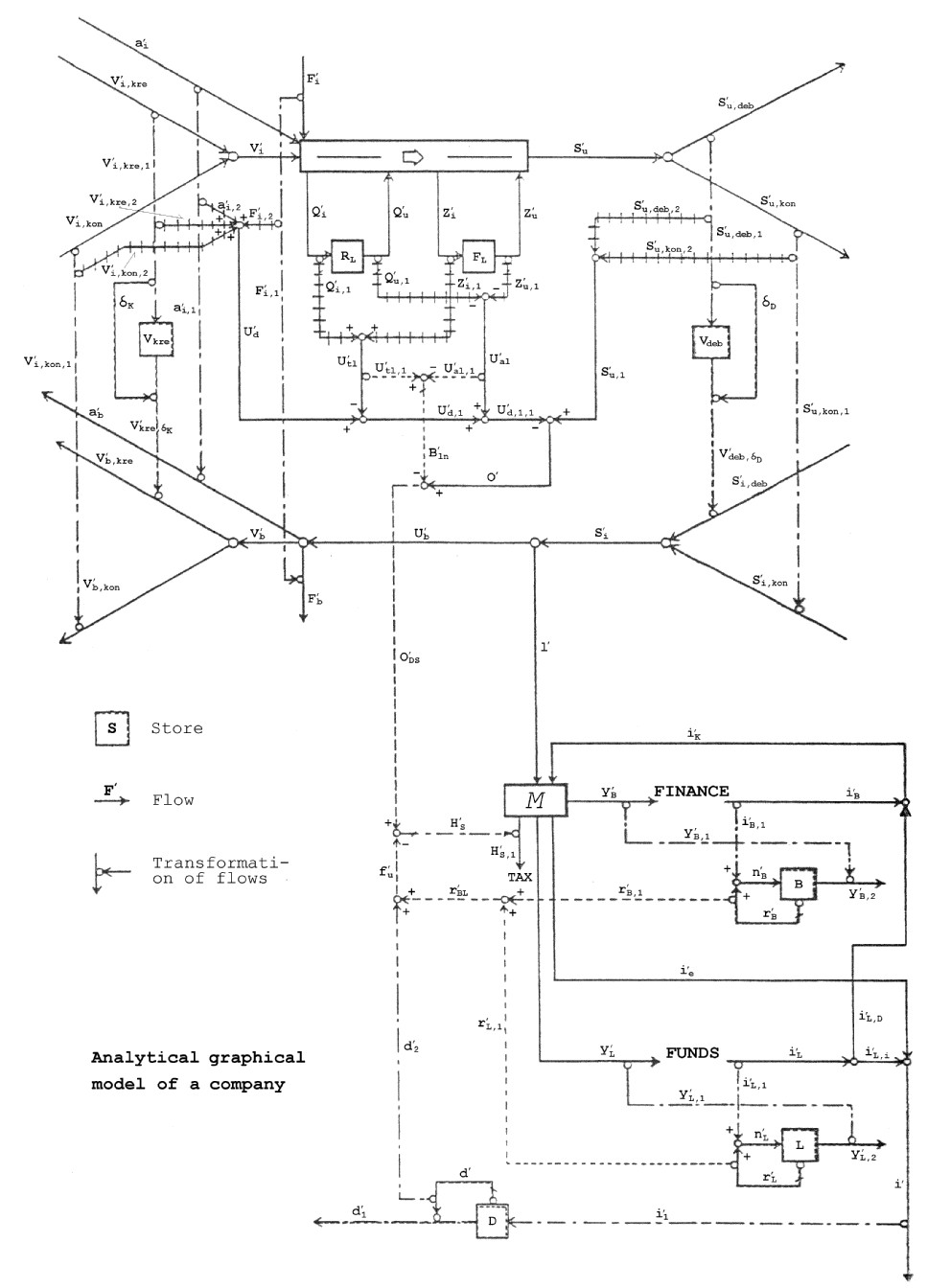

analytical graphical business model This

Chapter describes an analytical graphical business model (see Fig. 2.1.).

This model will form the basis of a mathematical analytical descrip- tion of

the business which can be used by the business management in their principal

planning activities. The model will integrate principal elements of

managerial economics and the accounting theory, under the assumption that the

business comprises an activity/ cash flow and related principal assets

(accounts payable, accounts receivable, inventories). It is the management's

task to achieve the best possible composition of this general structure by

using some of the ratios defined in the model. 2.1. Activity parameters 2.1.1. Sales The volume of goods sold by the firm per unit time

is denoted S'u, where S'u = S'u(t). The dot denotes the physial dimension of

“current”. Sales

are here divided into two main components of which one is the reference sales

S'u,kon, which refers to the share of

sales which is paid for in cash. The other component of sales is denoted with

S'u,deb, which refers to the share of sales

which is paid for by the trade accounts receivable the debit time dD after delivery from the firm. Here the following

eguation applies: S'u(t) = S'u,deb(t) + S'u,kon(t) (1) 2.1.2. Purchases The

firm is supplied with a number of labor hours per time unit denoted by a'i and with the volume of goods per time unit denoted

by V'i. The flow of goods consists of two main components

of which one is the reference purchase V'i,kon, and the other one in the goods purchased on credit

V'i,kre, which are

paid for by the firm after the credit time dK. - 4 –

- 5 - The

following equation applies: V'i(t) = V'i,kre(t) + V'i,kon(t) (2) The firm is supplied with the fixed volume of

resources per unit time F'i. This flow of resources may, for example, include

electricity, administration, heating, rent, etc. 2.1.3. Inventories The

volume Q'i of raw materials supplied per unit time is added to the raw materials inventory consisting

of the volume RL. From the

raw materials in- ventory is deduced the raw materials volume Q'u. The following equation appli- es here: t RL = ò (Q'i(t) - Q'u(t))dt (3) 0 The volume of finished goods per unit time Z'i is added to the finished goods inventory consisting of the volume FL. From the finished goods invento- ry is deduced the

finished goods volume Z'u. The following equation applies here: t FL = ò (Z'i(t) - Z'u(t))dt (4) 0 2.2. Payment parameters, operations 2.2.1. Sales The

total volume of means of payment per time unit from the customers is denoted

with S'i. This payments flow consists of two components. One

component is the payments flow S'i,kon caused by the cash sales flow S'u,kon. The other component S'i,deb is the payment flow caused by the credit sales flow

S'u,deb. Here the

following equation applies: S'i(t) = S'i,kon(t) + S'i,deb(t) (5) - 6 - 2.2.2. Purchases The

total volume of payment per unit time for operations is denoted by U'b. This payment flow is composed of three components,

a'b and V'b and F'b. a'b is the payment flow corresponding to the flow of

labour hours consumed a'i, V'b is the payment flow corresponding to the flow of

raw material purchases V'i, F'b is the payment flow corresponding to the flow of

fixed resources consumed F'i. The following equation applies: U'b(t) = a'b(t) + V'b(t) + F'b(t) (6) The

payments flow V'b is made up of two components. One component is the

pay- ments flow V'b,kon corresponding to the cash purchases of rawmaterials

V'i,kon; the other

component is the payments flow V'b,kre corresponding to the credit purchase of raw

materials V'i,kre. The following equation applies; V'b(t) = V'b,kon(t) + V'b,kre(t) (7) 2.3. Market parameters, sales In

order to depict the fundamental financial effects of the market on the firm

and its effects on earnings, the market is characterized by three basic

components q , p and dD. They also describe the fundamental link between

the firm's sales of goods and the related payment flows. 2.3.1. Cash sales ratio q The

cash sales ratio is defined by the equation: S'u,kon(t) = q S'u(t) (8) where

0 £ q £ 1

In

a manufacturing business q will typically have a value in the interval 0 £ q £ 0.2.

In a supermarket q will typically be in the interval 0.8 £ q £

1. - 7 - 2.3.2. The price p The

price of the firm's product(s) is defined by the eguations S'u,kon,1(t) = p S'u,kon(t) (9) S'i,kon(t) = S'u,kon,1(t) (10) where

S'u,kon,1(t) is the

flow of debts corresponding to the sales flow S'u,kon(t) (i.e. the current invoice flow stating the

amount of debt; see equation (9)). Equation (10) expresses the fact that the

flow of debts S'u,kon,1(t) is equal to the payments flow from the customers

(cash payment). In

practice, it should be noted that there is normally a time lag between

invoicing and sales. However, it has a temporary negative effect on liquidity

and the computation of results. Management will therefore have in view that

the invoicing is done without the mentioned delays. 2.3.3. Debit time dD This

model defines the debit time dD as the time of delivery of the goods from the firm

until the time of payment by the customer for the goods. In practi- ce, dD

is spread over the individual customers but with well defined terms of

payment the mean value can be detemined. The

definition of dD can be expressed by the equations S'u,deb,1(t) = p S'u,deb(t) (11) V'deb,dD(t) = S'u,deb,1(t - dD) (12) S'i,deb(t) = V'deb,dD(t) (13) - 8 - S'u,deb,1 refers here to the invoice flow corresponding to the

credit sales flow S'u,deb cf. equation (11). Equation (12) gives a functional

description of a function V'deb,dD(t), which can be defined as the payments flow (documents)

corresponding to the actual receipt of payments S'i,deb(t) cf. equation (13). In practice, no time lag is

found between the two last mentioned functions. In

pratice, attention should be paid to the fact that there may be a time lag in

the business between invoicing and sales, the result being changes in li-

quidity and the computation of earnings. Management usually aims at applying

equation (11) in practice, i.e. no time lag. 2.4. Market parameters, purchases With

a view to depicting the fundamental financial effects of the purchasing

market on the firm as well as its effects on costs, it is characterized by

four basic components e, q1,

q2 and dK. They describe the fundamental link between the

firm's purchases of resources and the related payment flows. 2.4.1. Cash purchases ratio e The

cash purchases ratio is defined by the equation: V'i,kon(t) = e V'i(t) (14) where

0 £ e £ 1 In,

say, a manufacturing business e will typically have a main value

in the interval 0 £ e £

0.2. This is also a typical

feature in a trading firm. 2.4.2. The price q1 of raw materials The

price of the firms raw materials is defined by the equation: - 9 - V'i,kon,1(t) = q1 V'i,kon(t) (15) V'b,kon(t) = V'i,kon,1(t) (16) where

V'i,kon,1(t) is the

flow of debts corresponding to the raw materials flow V'i,kon(t) (i.e. the current receipt of invoices stating

the amounts of debts); see equation (15). Equation (16) expresses the fact

that the flow of debts V'i,kon,1(t) is equal to the payments flow to suppliers (cash

payment). In

practice, attention should be paid to the fact that the time lag between the

supplier's invoicing and the supplies of raw materials is usually a temporary

feature which has a temporary positive effect on liquidity and the

computation of results. 2.4.3. The price q2 of labor hours The

price of the firm's labor hours is defined by the equations a'i,1(t) = q2 a'i(t) (17) a'b(t) = a'i,1(t) (18) where

a'i,1(t) is the

time ticket flow corresponding to the flow of labor hours used a'i(t) (i.e. the current issuing of time tickets

stating wages earned); see equation (17). Equation (18) expresses the fact

that the time ticket flow a'i,1(t) is equal to the time rate flow a'b(t). In

practice there is a certain time lag between functions on the right hand side

and the left hand side of the equal sign in equation (17). This time lag is

ignored here. There is usually no time lag between the functions of equa-

tion (18), or the time lag is relatively small and of no importance here. - 10 - 2.4.4. Credit time dK This

model defines the credit time dK as the time from the time of delivery of the raw

materials to the firm until the time of payment by the firm for the raw

materials. In practice, dK is spread over the individual suppliers but with

well defined terms of payment the mean value can be used. The definition of dK

can be expressed by the equations: V'i,kre,1(t) = q1 V'i,kre(t) (19) V'kre,dK(t) = V'i,kre,1(t - dK) (20) V'b,kre(t) = V'kre,dK(t) (21) where

V'i,kre,1(t) refers

here to the invoice flow corresponding to the credit purchases flow V'i,kre(t), cf. equation (19). Equation (20) gives a

functional description of a function V'kre,dK(t) which can be defined as the payment order flow

(documents) corresponding to the actual effecting of payments V'b,kre(t), cf. equation (21). In practice, there is no

time lag between the two last mentioned functions. In practice, attention should be

paid to the fact that the time lag between the supplier's invoicing and the

supplies of raw materials is usually a temporary feature which has a

temporary positive affect on liquidity and the computation of results. The

following equations are defined in relation to the fixed resources consumed F'i and the related fixed costs F'b. F'i,1(t) = k F'i(t) (22) F'b(t) = F'i,1(t) (23) - 11 - where

F'i,1(t) in

equation (22) refers to the flow of debts in the form of in- voices (stating

amounts) corresponding to the fixed resources flow F'i(t). k denotes a symbolic operator in the

form of an average price of the fixed re- sources unit. In practice, there is

some time lag between the functions in eguation (23). As, however, the fixed

costs by definition are constant in ti- me, such a time lag is not important

in this context. 3.1 Income statement In

this Chapter an income statement for operations is presented (before depre-

ciation, etc.) using the general main principles of accounting theory. 3.1.1 Sales of goods Sales

of goods are defined on the basis of the following equations: S'u,kon,2(t) = S'u,kon,1(t) (24) S'u,deb,2(t) = S'u,deb,1(t) (25) S'u,1(t) = S'u,kon,2(t) + S'u,deb,2(t) (26) Eguation

(24) expresses the fact that the flow of debts (in the form of in- voices

with statement of amounts) S'u,kon,1(t) gives rise to an equally large information flow

S'u,kon,2(t). This quantity

is identical with the current crediting to the cash sales account. From

equation (25) follows that the flow of debts S'u,deb,1(t) causes an equally large information flow S'u,deb,2(t). This quantity is identical to the current

crediting to the credit sales account. Total

sales in the form of the information flow S'u,1(t) corresponding to the total crediting to the

sales account are then obtained from equation (26). - 12 - 3.1.2 Costs The

costs of the firm in connection with production and sales are defined by the

following equations: V'i,kon,2(t) = V'i,kon,1(t) (27) V'i,kre,2(t) = V'i,kre,1(t) (28) a'i,2(t) = a'i,1(t) (29) F'i,2(t) = F'i,1(t) (30) U'd(t) = V'i,kon,2(t) + V'i,kre,2(t) + a'i,2(t) + F'i,2(t)

(31) Equation

(27) expresses the fact that the invoice flow from the cash purchase V'i,kon,1(t) is currently debited to the cash purchases

account to the extent of the cash flow V'i,kon,2(t). Equation

(28) expresses the fact that the invoice flow from the credit pur- chase V'i,kon,1(t) is currently debited to credit purchases account

to the extent of the cash flow V'i,kre,2(t). Equation

(29) denotes the functional relationship between the time ticket flow a'i,1(t) and the current debiting to the time rate

account of the wage payment flow a'i,2(t). Equation

(30) expresses the functional relationship between the invoice flow F'i,1(t) for fixed costs and the current debiting of the

cash flow F'i,2(t) to the fixed costs account. The

total cost flow is defined by equation (31). - 13 - 3.1.2.1 Inventories, additions (with signs)

By

way of introduction, it is mentioned that the signs relating to additions to

inventories (as a mean time value) are assumed to be the same as those

relating to additions to sales (as a mean time value). Against this

background the ad- ditions to the individual inventories will for principal

planning purposes ha-ve the same signs. The inventories only serve as

"standby stores" in case of emergency events "i.e. in normal

operation state" the materials and products go directly through the

factory. Thus, the following systems of equations apply: The

increase of sales S'u is supplied directly by the production and the

inventories are increased proportionally with S'u. Q'i(t) > 0 Q'u(t) = 0 d S'u ¾¾¾¾ >

0 Þ

(32) dt Z'i(t) > 0 Z'u(t) = 0 Constant

sales S'u is supplied directly by the production and the

inventories remain constant.

Q'i(t) = 0 Q'u(t) = 0 d S'u ¾¾¾¾ =

0 Þ

(33) dt Z'i(t) = 0 Z'u(t) = 0 The

decrease of sales S'u is supplied directly by the production and the flow

from inventories. The inventories are decreased proportionally with S'u. - 14 - Q'i(t) = 0 Q'u(t) > 0 d S'u ¾¾¾¾ < 0 Þ (34) dt Z'i(t) = 0 Z'u(t) > 0 The

system of equations (32) denotes that inventories rise when sales rise. The

system of equations (33) denotes that inventories are constant when sales

remain unchanqed. The

system of equations (34) denotes that inventories fall when sales fall. Based

on these main principles for the model the following equations can be

developed. Q'i,1(t) = qR Q'i(t) (35) Q'u,1(t) = qR Q'u(t) (36) Z'i,1(t) = qF Q'i(t) (37) Z'u,1(t) = qF Z'u(t) (38) U'tl(t) = Q'i,1(t) + Z'i,l(t) (39) U'al(t) = Q'u,1(t) + Z'u,1(t) (40) where Q'i,1(t) is the flow

of additions to raw materials invento-

ries corresponding to the additions to rawmateri-

als inventory records with statement of amounts. - 15 - Q'u,1(t) is the

flow of deductions to raw materials inven-

tories corresponding to the deductions to raw

materials inventory records with statement of

amounts. Z'i,1(t) is the

flow of additions to finished goods inven-

tories corresponding to the additions to finished

goods inventory records with statement of amounts. Z'u,1(t) is the

flow of deductions to finished goods inven-

tories corresponding to the

deductions to finished

goods inventory records with statement of amounts. qR denotes the calculated rav material price per

unit

of finished goods. qF denotes the calculated direct cost price per

unit

of finished goods. U'tl(t) is

total additions to inventories. U'al(t) is

total deductions from inventories. The

system of equations (32), (33) and (34) can now be given the form: d S'u ¾¾¾¾ > 0 Þ U'tl(t) > 0

and U'al(t) = 0

(41) dt d S'u ¾¾¾¾ = 0 Þ U'tl(t) = 0

and U'al(t) = 0

(42) dt d S'u ¾¾¾¾ < 0 Þ U'tl(t) = 0

and U'al(t) > 0

(43) dt Attention

is drawn to the fact that the physical model based on the FIFO principle can

be desribed mathematically only by - 16 - d S'u sign ( ¾¾¾¾ ) = sign (U'tl(t)) (44) d t given

U'al(t) = 0

(45) and

U'tl(t) is

computed with signs. 3.1.3. Resourceconsumption (incl. F'i,1) Resources

consumed U'd,1,1(t) can be defined by the following equations: d S'u ¾¾¾¾ > 0 Þ U'd,1,1(t) = U'd(t) - U'tl(t)

(46) dt given U'al(t) = 0 d S'u ¾¾¾¾ = 0 Þ U'd,1,1(t) = U'd(t) (47) dt d S'u ¾¾¾¾ < 0 Þ U'd,1,1(t) = U'd(t) + U'al(t)

(48) dt

given U'tl(t) = 0 3.1.4. Operation profit (before interest and

depreciation) The

operating profit (before interest and depreciation etc.) is defined by the

equation: O'(t) = S'u,1(t) - U'd,1,1(t) (49) 3.1.5 Operating profit incl. inventory

depreciation If a tax year of the length T is considered in a

period of time t1

£ t £ t1

+ T where t1 is a time

selected at random, the following functions can be defined: t1+T Vkøb = ò q1 V'i(t) dt (50) t1 w

= w(t1) (51) an = an(t) (52) - 17 - In

equation (50) Vkøb represents

the purchases of goods in the period

t1 £ t £ t1 + T. Equation

(51) defines w(t1) as the

total inventory value at time t1.

an(t) in the equation defines the inventory

depreciation rate. Materials

consumed computed for tax purposes is then derived from the follow- ing

equation (53): Vtax = Vkøb + w(t1) - (w(t1)/(1 - an(t1)) t1+T + ò (U'tl(t) - U'al(t)) dt) (1 - an(t1 + T)) (53) t1

For

principal planning purposes the mean time value of an(t)

for a given business will be a constant an and limited i.e. 0

< an < 0.3 . Based on this assumption equation (53)

gives

t1+T Vtax = Vkøb - (1 - an) ò (U'tl(t) - U'al(t)) dt (54) t1 Materials

consumed for operations is defined by the following equation:

t1+T Vdrift =

Vkøb + w(t1) - (w(t1) + ò (U'tl(t) - U'al(t)) dt)

(54a) t1 or t1+T Vdrift =

Vkøb - ò (U'tl(t) - U'al(t)) dt) (55) t1 If

equation (55) and equation (54) are combined, the following equations are

developed: t1+T Vtax = Vdrift + an ò (U'tl(t) - U'al(t)) dt (56)

t1 - 18 -

t1+T Vtax = Vdrift + ò an(U'tl(t) - U'al(t)) dt (57) t1

On

the basis of equation (57) the following functions can be defined: U'tl,1(t) = U'tl(t) (58) U'al,1(t) = U'al(t) (59) In

equation (58) U'tl,1(t) denotes total additions to inventories from a

taxation point of view. U'al,1(t) denotes in equation (59) total deductions from

invento-ries from a taxation point of view. With

the following definition equation: B'ln(t) = an (U'tl,1(t) - U'al,1(t)) (60) equation

(57) can be transformed into

t1+T Vtax = Vdrift + ò B'ln(t) dt (61) t1

On

the basis of equation (61) the following equation (62) can be defined: O'DS = O' - B'ln (62) where

O'DS is the

operating profit adjusted for inventory depreciation. 4.1. Change in liquidity (operations) The

cash flow released by operations, the change in liquidity, is defined by the

following equation (63): l'(t) = S'i(t) - U'b(t) (63) -

19 - 5.1. Cash balance The

cash balance of the firm is designated by M, which, in relation to the

present principal planning model, is very small in practice, i.e. M(t) = 0.

The folloving equation can now be developed: i'e = l' + i'K - y'B - y'L - H'S,1 (64) where

i'e is the

self financing flow y'B is the

service of bank loans y'L is the

service of other loans i'K is

current raise of loans for operations H'S,1 is tax

payments 5.2. Bank loans. The

firm is financed currently by trading credits in the form of the cash flow i'B. The equation is defined as follows: i'B,1(t) = i'B(t) (65) where

i'B,1(t) is the

information flow in the form of loan documents with statement of amounts

corresponding to the cash flow i'B(t). The bank charges currently interest r'B(t) on the amount outstanding B

= B(t) where r'B(t) is the document flow with statement of interest.

The following equation applies: n'B(t) = i'B,1 + r'B (66) where

n'B(t) is the

firm's current crediting to the bank account. - 20 - The

current service payments y'B(t) to the bank give rise to a payment order flow

with statement of amounts y'B,1(t). We have: y'B,1(t) = y'B(t) (67) The

payment order flow y'B,1(t) involves a corresponding current debiting to the

bank account in the form of y'B,2(t). The following equation therefore ap- plies: y'B,2(t) = y'B,1(t) (68) 5.3. Loans (long term) The

long term financing of the business is represented by the cash flow i'L. The following equation applies: i'L,1(t) = i'L(t) (69) where

i'L,1(t) is the

information flow in the form of loan documents with statement of amounts

corresponding to the cash flow i'L(t). On the loan L current interest r'L(t) is charged where r'L(t) is the document flow with statement of interest.

The following equation applies: n'L(t) = i'L,1(t) + r'L(t) (70) where

n'L(t) is the

firm's total current crediting to the loan account. The

following equation applies: i'L(t) = i'L,1(t) + i'D(t) (71) where

i'L,D(t) denotes

the long term financing flow to the working capital, and i'L,1(t) is the long term financing flow to the fixed

capital. - 21 - The

folloving equation applies: i'K(t) = i'B(t) + i'L,D(t) (72) The

current service payments y'L(t) to lender give rise to a payment order flow with

statement of amounts y'L,1(t). We have y'L,1(t) = y'B(t) (73) The

payment order flow y'L,1(t) involves a corresponding current debiting to the

loan account in the form of y'L,2(t). The following equation therefore applies: y'L,2(t) = y'L,1(t) (74) 6.1. Investment (in fixed capital) The

firm's current investment in fixed capital is denoted i'(t). The following equation applies: i'(t) = i'L,1(t) + i'e(t) (75) It

is pointed out that, in practice, i'L,D(t) currently converts short term liabilities into

long term liabilities, which means that at a strategic level alone i'L,D = 0. As to i'e(t), there is no unique definition of i'e(t) as it de- pends on the financing and market

situation. Roughly speaking, i'e(t) is the average cash flow which can be withdrawn

from the business without changing the existing product, investnent and

financing structure and the necessary financial reserves set aside for an

appropriate future development of the bu- sinees. - 22 - 7.1. Depreciation (for tax purposes) It

is normal to distinguish between depreciation for tax purposes and depre-

ciation for accounting purposes. Depreciation for accounting purposes is used

with the object of comparing alternative projects on the basis of special

cost principles. These principles are purely OR mathematical models and do

not reflect the physical business situation. Here

we shall only take an overall view of the financial flow of the firm for

which reason depreciation for tax purposes will be used. Such depreciation

will only reflect the actual effects on liquidity (after tax). The

following equations apply: i'1(t) = i'(t) (76) t D(t) = ò (i'1(t) - d'1(t))dt (77) 0 where

i'1(t)

represents the current debiting to the tax depreciation account corresponding

to the investment flow i'(t). d'1(t) is the current crediting to the same account

(i.e. current "depreciation"). D(t)

represents the balance of the tax depreciation account. The depreciation

charges d'(t)

are calculated on the basis of this account, and the following expressions

apply: d'1(t) = d'(t) (76a) d'2(t) = d'(t) (76b) where

d'2(t) is the

depreciation flow which is included on the basis of compu- tation of the

taxable income. - 23 - 8.1. Interest (for tax puroses) Interest

is usually computed for two main purposes. One concerns the income statement

for tax purposes, the other concerns internal computation purposes such as

the effect of interest on the income statement as a whole or in con- nection

with special computations. No

distinction will be made here between the two purposes. The interest charges

will be placed in this model with the sole aim of depicting the fundamental

fi-nancial characteristics. The

following equations are defined: r'B,1(t) = r'B(t) (78)

r'L,1(t) = r'L(t) (79) r'BL(t) = r'B,1(t) + r'L,1(t) (80) where r'B,1(t) denotes the current recording of interest

payment to the bank. r'L,1(t) denotes the current recording of interest

payments to other lenders. The recording of total interest payments is

designated r'BL(t). 9.1. Tax payments According

to the principles governing computation of the taxable income the following

equations apply: f'u(t) = d'2(t) + r'BL(t) (81) H'S(t) = s (O'DS(t) - f'u(t)) (82) H'S,1(t) = H'S(t) (82a) - 24 - where

f'u(t) is a

state function for the computation of tax, cf. equation (81), s is the

tax rate, H'S(t) is the computed tax payment and H'S,1(t) is the tax payment flow. 10.1. Principal ratios As

appears from Fig. 2.1, the following principal ratios in the firm are

im-portant to the understanding of the dynamic (tactical) characteristics of

the firm. Operating profit O'(t) Change in liquidity l'(t) Working capital (net) K'(t) Contribution ratio DG(t) Depreciation d'2(t) Interest r'BL(t) These

ratios will be discussed in detail in the following. 10.1.1. Operating profit O'(t)

Using

different assumptions concerning prices and changes in principal assets

(accounts payable, accounts receivable, inventories) it is possible via Fig.

2.1 to assess the effects on the operating profit. A reduction of the raw

materials inventories in a situation with raw materials prices which are

higher than the prices of the raw materials inventories but otherwise

constant will increase the profit temporarily in the period concerned. One

of the things that will be seen is that the profit O'(t) is independent of the volume of trade accounts

payable and the volume of trade accounts recei- vable. - 25 - 10.1.2. Change in liquidity l'(t)

Other

things being equal, the following expression, cf. Fig. 2.1., applies: d S'u ¾¾¾¾ > 0 Þ l'(t) < O'(t) (83) d t Equation

(83) shows that the profit O'(t) is larger than the change in liqui- dity in the

case of growing sales in the firm, the reason being the funds ti- ed up,

calculated with signs, in principal assets (accounts receivable and

inventories), d S'u ¾¾¾¾ = 0 Þ l'(t) = O'(t) (84) d t Equation

(84) shows that the change in liquidity is equal to the profit in the case of

constant sales, the reason being an unchanged volume of principal as-sets

(accounts payable, accounts receivable and inventories). d S'u ¾¾¾¾ < 0 Þ l'(t) > O'(t)

(85) d t From

equation (85) appears that in the case of falling sales the change in

liquidity becomes greater than the operating profit owing to a reduced volume

of principal assets (accounts payable, accounts receivable and inventories). The

above shows how important it is for the business to keep the cash budget

currently up to date as the profit and the financial circumstances of the

business may differ substantially from each other. It should be noted that if

the net principal assets are negative, the inequality signs in (83) and (85)

must be reversed. - 26 - 10.1.3. Working capital K(t) If

the working capital is denoted K(t), the definition eguation for net capi-

tal tied up in the operating system will apply: K(t)

= Vdeb(t) + FL(t) + RL(t) - Vkre(t) (86) The

following definition equation will also apply: d K(t) ¾¾¾¾ + l'(t) = O'(t) (87) d t Equation

(87) shows that the profit is equal to the change in liquidity + the

increment of the net working capital tied up. If

equation (87) is transformed, the following equation is derived: d K(t) ¾¾¾¾ = O'(t) - l'(t) (88) d t Equation

(88) denotes that the difference between the operating profit and the change

in liquidity is equal to the financing requirements for operations in the

period under review. 10.1.4. Contribution ratio DG(t) The

contribution ratio is defined by equation (89): DG(t)

= (O'(t) + F'b(t))/S'u,1(t) (89) Equation

(89) shows that DG is independent of the amount of sales and defines the

share of sales which will cover fixed costs, etc. The point is stressed here

that a high contribution ratio does not imply that there is "money"

to cover the fixed costs. For further details see section 10.1.2. as the size

of l'(t)

gives only an indication of the ability of the firm to pay fixed costs, etc. - 27 - 10.1.5. Depreciation Depreciation

contributes to influencing the firm's liquidity, cf. equation (82). Assuming

that the investments are made as individual projects at time intervals, it is

shown that depreciation in the periods between investments causes liquidity

to rise owing to the reduction in tax payments. However,

it should be noted that of the cash flow released after tax there must be

funds to cover repayment commitments in connection with loans raised. The

effect of the cash flow released after tax described above is therefore

partial and must be seen in relation to the repayment commitments. Later

there will be shown that for practical reasons the division described here is

desirable for the understanding of the financial components of the cash flow

released. 10.1.6. Interest r'BL From

Fig. 2.1 and from equations (81) and (82) is apparent that interest pay-ments

reduce the cash flow released after tax. Thus, the net effect on cash flow released (to be defined

later) stems partly from the computation of income for tax purposes, partly

from the payment of interest on total loans. The

computation of interest on total loans seen in relation to a given level of activity

will be defined later. - 28 - 11. An analytical mathematical business

model This

Chapter presents a new analytical mathematical model description of the

business. This model has been developed for use in the tactical planning pro-

cess. No reference can be made to a similar model in existing literature. The

theoretical literature which gets nearest is S. Eilon's article discussed in

Chapter A in “Economical Keynumbers”. 11.1. Physical and financial functions in the

operating system In

the following further definitions of mathematical functions and their rela-

tionships will be established. The sole justification of these definitions is

that they provide the basis of a clear and generally coherent system of

equa-tions between ratios. 11.1.1. Sales A

basic sales volume is defined: S'u0 = S'u(0) (90) where

S'u0 is the

volume of sales S'u at time t = 0, i.e. at the beginning of the

simulation period. The

development of sales during the time period is defined by equation (91): d S'u(t) ¾¾¾¾

= as S'u0 (91) d t where

as is constant. - 29 - The

following equation now applies: S'u(t) = S'u0(1 + as t) (92) where

t ³ 0 11.1.2. Inventories Let

a ratio hF be defined

so that equation (93) applies: hF = FL(t)/S'u(t)

(93) for

t ³ 0, hF being a positive constant which is designated

"finished goods inventory time". Another ratio hR is defined so that equation (94) applies: hR = RL(t)/S'u(t) (94) for

t ³ 0 being a

positive constant which is designated "raw materials inventory

time". From

equation (93) follows: FL(t) = hF S'u(t) (95) The

definition equation applies: t FL(t) = FF(0) + ò Z'i(t) dt (96)

0 which

substituted into equation (95) gives: |

|

- 30 - t FL(0) + ò Z'i(t) dt = hF S'u(t) (97) 0 or

t ò Z'i(t) dt = hF S'u(t) - FL(0) (98) 0 If

equation (92) is used in equation (98), the following expression is derived: t ò Z'i(t) dt = hF S'u0 as t + (hF S'u0 - FL(0)) (99) 0 For

t = 0 equation (93) gives the following expression: hF = FL(0)/S'u(0) (100) Using

equation (100) together with equation (99) we have: t ò Z'i(t) dt = hF S'u0 as t (101) 0 The

solution to the integral equation (101) is: Z'i(t) = hF S'u0 as

(102) The

flow of goods Z'i(t) to the finished goods inventory may then be

defined by equations (103) and (104): Z'i(t) = hF S'u0 as

(103) for

as ³ 0 and

- 31 - Z'u(t) = - hF S'u0 as

(104) for

as < 0 Mathematically

the physical equations (103) and (104) may be described by equation (105) for

all values of as, i.e. Z'i(t) = hF S'u0 as

(105) for - ¥ < as < ¥ With

equation (105) the physical inventory system has been converted to a

mathematical model where Z'i(t) can change sign and where Z'u(t) = 0 for all t, cf. equation (102). From

equation (94) follows: RL(t) = hR S'u(t) (106) The

definition equation applies:

t RL(t) = RL(0) + ò Q'i(t) dt (107)

0 which

combined with equation (106) gives: t RL(0) + ò Q'i(t) dt = hR S'u(t) (108) 0 or

t ò Q'i(t) dt = hR S'u(t) - RL(0) (109) 0 If

equation (92) is used in equation (109), the following equation is derived: - 32 - t ò Q'i(t) dt = hR S'u0 as t + (hR S'u0 - RL(0)) (110) 0

For

t = 0 equation (94) gives: hR = RL(0)/S'u(0) (111) Using

equation (110) together with equation (111) we have: t ò Q'i(t) dt = hR S'u0 as t

(112) 0 The

solution to the integral equation (112) is: Q'i(t) = hR S'u0 as

(113) The

flow of goods Q'i(t) to the raw materials inventory can now be

defined by equations (114) and (115): Q'i(t) = hR S'u0 as

(114) for

as ³ 0 Q'u(t) = - hR S'u0 as (115) for

as < 0 Mathematically

the physically equations (114) and (115) can be described by equation (116)

for all values of as,

i.e. Q'i(t) = hR S'u0 as

(116) for - ¥ < as < ¥ With

equation (116) the physical inventory system has been converted to a

ma-thematica1 model where Q'i(t) can change sign and where Q'u(t) = 0 for all t. - 33 - 11.1.3. Output Total

output T'p(t) is given by: T'p(t) = S'u(t) + Z'i(t) (117) If

the ratio ba is here

defined as the number of labor hours used per unit of output and the ratio bR as the raw materials consumption per unit of

finished goods, the equations, resource balance equations, will apply: a'i(t) = ba T'p(t) (118) V'i(t) = bR T'p(t) + Q'i(t) bR (119)

If

equation (117) and equation (119) are combined, the following equation is

obtained: V'i(t) = bR S'u(t) + bR Z'i(t) + Q'i(t) bR (120) If

equations (92), (105) and (116) are substituted into equation (120), the

following equation is obtained: V'i(t) = bR S'u0 (1 + (hF + hR + t) as) (121) Using

equations (117), (92) and (105), equation (118) gives: a'i(t) = ba S'u0 (1 + as(t + hF)) (121a) 11.1.4. Sales, ingoing payments Using

equations (8), (9) and (10) we obtain payments derived from cash sales: S'i,kon(t) = p q S'u0 (1 + as t) (122) - 34 - Using

equations (1), (8), (11), (12) and (13) we obtain payments derived from debit

sales: S'i,deb(t) = p (1 - q) S'u0 (1 + as(t - dD)) (123) Equations

(1), (122) and (123) give: S'i(t) = p q S'u0 (1 + as t) + p (1 - q) S'u0 (1 + as(t

- dD)) (124) or

S'i(t) = p S'u0 (1 + as(t - dD(1 - q))) (125) 11.1.5. Purchases, outgoing payments The

outgoing payments flow corresponding to cash purchases of raw materials is

expressed by means of equations (14), (15), (16) and (121) as V'b,kon(t) = q1 e bR S'u0 (1 + (hF + hR + t)as) (126) Credit

purchases of raw materials cause an outgoing payments flow which by means of

equations (7) (14), (19), (20) and (21) is computed at: V'b(t) = e q1 V'i(t) + (1 - e)q1 V'i (t - dK) (127) Equation

(127) is transformed by means of equation (121) into: V'b(t) = e q1 bR S'u0(1 + (hF + hR + t) as) + (1 - e)q1

bR S'u0(1 + (hF + hR

+ t - dK)as) (128) Equation

(128) is reduced to: V'b(t) = q1 bR S'u0(1 + as(hF + hR + t - dK (1 - e))) (129) - 35 - The

total payments flow to purchases of resources is then obtained by using

equations (6), (17), (18) and (129): U'b(t) = q2 a'i(t) + q1 bR S'u0(1 + as (hF + hR + t - dK (1 - e))) + F'b(t) (130) By

combining equation (121a) and equation (130) the total outgoing payments flow

is then given by: U'b(t) = S'u0(q2

ba (1 + as (t + hF))

+ q1 bR(1

+ as (hF + hR + t - dK(1 - e))) + F'b(t) (131) 11.1.6. Change in liquidity The

accounting concept, change in liquidity l'(t), here also called cash flow, can then by the use

of equations (63), (125) and (131) be given the following form: l'(t) = S'u0(p(1 + as(t - dD(1 - q))) - q2

ba (1 + as(t + hF))

- q1 bR(1

+ as

(hF + hR + t - dK(1 - e)))) - F'b(t)

(132) 11.2. Capital tied up in the operating system

Depending

on the firm's level of activity capital will be tied up in the ope- rating

system. Capital will be tied up in trade accounts payable, raw materi- als

inventories and finished goods inventories as well as accounts receivable

(the amounts are indicated with signs). 11.2.1. Trade accounts receivable The

volume of trade accounts receivable is defined by the following equation,

equations (1), (8), (11) and (12) being used: dD Vdeb(t) = ò p(1 - q)S'u(t - x) dx (133) 0 - 36 - In

this model it is assumed that equation (92) applies. From this equation

combined with (133) follows: dD Vdeb(t) = p(1 - q) S'u0 ò (1 - as(t - x)) dx (134)

0 The

computation of the integral in equation (134) allows equation (134) to be

reduced to: Vdeb(t) = p(1 - q) S'u0 dD (1 + as(t - 0.5 dD)) (135) 11.2.2. Trade accounts payable The

volume of trade accounts payable is defined by the following equation,

equations (2), (14), (19) and (20) being used: dK Vkre(t) = ò q1 bR(1 - e) V'i(t - x)) dx (136) 0 Assuming

that sales satisfy equation (92) and that equation (121) applies, equation

(136) develops the following expression: dK Vkre(t)

= q1 bR(1

- e) S'u0 ò (1 + as(hF + hR

+ t - x)) dx (137) 0 By

computing the integral in equation (137) this equation is reduced to: Vkre(t) = q1 bR(1

- e) S'u0 dK (1 + as(hF

+ hR + t - 0.5 dK))

(138) l1.2.3 Raw materials inventory The

volume of the raw materials inventory is given by equation (106). The value

of the raw materials inventory RL,1(t) satisfies the equation: RL,1(t) = q1 bR RL(t)

(139) - 37 - If

equations (106) and (92) are substituted into equation (139), we have: RL,1(t) = q1 bR hR S'u0(1 + as t) (140) 10.2.4. Finished goods inventory The

volume of the finished goods inventory is given by equation (95). The

calculated consumption of materials and labor hours per unit of finished

goods is given by qF,

cf. equation (37). The definition equation applies: qF = bR

q1 + ba

q2 (141) The

value of the finished goods inventory FL,1(t) satisfies the equa-ion: FL,1(t) = qF FL(t) (142) If

equations (95), (92) and (141) are substituted into equation (142), the

following expression is obtained: FL,1(t) = (bR q1 + ba q2) hF S'u0(1 + as t) (143) 11.2.5. Working capital (tied up in the

operating system) The

total capital tied up in the operating system, i.e. the working capital K(t),

is through the use of equations (135), (138), (140) and (143) given by: K(t)

= Vdeb(t) - Vkre(t) + RL,1(t) + FL,1(t) (144) or

by substituting into the relevant places K(t) = p(1 - q)S'u0 dD (1 + as(t - 0.5 dD)) - q1 bR (1 + e)S'u0 dK (1 + as(hF + hR + t - 0.5 dK)) + q1 bR hR S'u0(1 + as t) + (bR

q1 + ba

q2) hF

S'u0(1 + as t) or - 38 - K(t) = S'u0(1 + as

t)(hF (bR

q1 + ba

q2) + q1

bR hR)

+ p(1

- q) dD S'u0(1 + as(t

- 0.5 dD)) - q1 bR

(1 - e) dK S'u0(1 + as(hF + hR + t - 0.5 dK))

(145) 12.1. Operating profit (for accounting

purposes) In

the following, functions are established for the computation of operating

profit based on accounting theory. The

turnover of the firm is obtained by using equations (9), (11), (24), (25) and

(26) and is expressed as: S'u,1(t) = p S'u(t) (146) Using

equation (92) and equation (136) gives: S'u,1(t) = p S'u0(1 + as t) (147) Raw

materials consumed corresponding to sales S'u(t) are given by the equation: V'for(t) = q1 bR S'u(t) (148) or

by using equation (92): V'for(t) = q1 bR S'u0(1 + as t) (149) The

wages paid, time rates, corresponding to sales S'u(t) are given by the equation: a'for(t) = q2 ba S'u(t) (150) or by using equation (92) a'for(t) = q2 ba

S'u0(1 + as t) (151) - 39 - By

using equations (147), (149) and (151) the operating profit O'(t) can now be given the form: O'(t) = S'u,1(t) - V'for(t) - a'for(t) - F'b(t) (152) or

O'(t) = S'u0(1 + as

t)(p - (q1 bR + q2

ba)) - F'b

(153) 12.2. Operating profit (computed on the basis

of Fig. 2.1) In

this section the operation profit will as an alternative be computed directly

on the basis of Fig. 2.1. The

costs U'd(t) in connection with sales S'u(t) are given by equation (31). If equations (2),

(15), (17), (19), (22), (23), (27), (28), (29), (30), (121) and (121a) are

substituted into equation (31), the following equation is de veloped: U'd(t) = q1 bR

S'u0(1 + (hF + hR

+ t) as) + q2 ba

S'u0(1 + (hF + t)as)

+ F'b (154) Computed

with a plus or minus sign (positive for inventory) the following va- lue is

added to the raw materials inventory, cf. equation (35): Q'i,1(t) = q1 bR Q'i(t) (155) or

equation (116) may be used: Q'i,1(t) = q1 bR

hR S'u0 as

(156) Here

the definition equation for cost prices of raw materials per unit of finished

goods has been used: qR = q1

bR (157) - 40 - The

following value is added to the finished goods inventory, cf. equation (37): Z'i,1(t) = qF Z'i(t) (158) or

equation (102) may be used: Z'i,1(t) = (q1 bR

+ q2 ba)

hF S'u0 as (159) The

total value flow to inventories now amounts to, cf. equations (44) and (45): U'tl(t) = q1 bR

hR S'u0 as

+ (q1 bR

+ q2 ba)

hF S'u0 as (160) or

by reduction U'tl(t) = S'u0 as(q1 bR

hR + (q1 bR

+ q2 ba)

hF) (161) The

total operating profit is obtained by using equations (147), (154) and (161)

and is expressed as: O'(t) = S'u(t) - (U'd(t) - U'tl)) (162) or

by substituting into the right hand side: O'(t) = p S'u0(1 + as t) - (q1

bR S'u0(1 + (hF + hR

+ t) as) + q2 ba

S'u0(1 + (hF + t) as) + F'b - S'u0 as

(q1 bR

hR + (q1 bR

+ q2 ba)

hF))

(163) - 41 - or

by reduction: O'(t) = S'u0(1 + as t)(p -(q1 bR + q2 ba)) - F'b

(164) It

will be seen that equations (153) and (164) are identical, i.e. a systema- tic

use of Fig. 2.1. gives here the same result as the use of a simple

"logi- cal" accounting method. 12.2.1. Operating profit incl. inventory

depreciation If

equations (161) and (58) are substituted into equation (60), U'tl,1(t) being computed with a plus or minus sign, the

following equation is obtained: B'ln(t) = an S'u0 as (q1

bR hR

+ (q1 bR

+ q2 ba)

hF)

(165) The

operating profit incl. inventory depreciation is given by equation (62). If equations

(164) and (165) are substituted into this equation, the following expression

is derived: O'DS(t) = S'u0(1 + as

t)(p -(q1 bR + q2

ba)) - F'b -

an S'u0 as (q1

bR hR

+ (q1 bR

+ q2 ba)

hF)

(166) or by reduction: O'DS(t) = S'u0((1 + as t)(p -(q1 bR

+ q2 ba)) - an as (q1

bR hR

+ (q1 bR

+ q2 ba)

hF) - F'b (166a) - 42 - 12.3.1. Bank loans This

model takes as its starting point that the net working capital tied up K(t)

can be given the form: K(t)

= K0 + Kinc(t)

(167) where

K0 is the net working capital tied up at time t = 0,

and Kinc(t) is the

change in the working capital tied up at time t. It is assumed that equation

(168) applies: d Kinc(t) ¾¾¾¾¾ = i'B(t) (168) d t This

means that the increase in the capital tied up in the operating system is

financed by the bank overdraft. If

equation (168) is used together with equation (167), the following equation

will also apply: d K(t) ¾¾¾¾¾ = i'B(t) (168a) d t It

is assumed that: B(0)

= 0 (169) This

means that the overdraft amounts to DKK B(0) = 0 at time t = 0. As

regards the mathematical model it is pointed out that in equation (168) i'B(t) may be both positive and negative as it is also

assumed here that, besides equations such as (65), (66), (67) and (68), the

following equation applies: y'B(t) = r'B(t) (170) - 43 - 12.3.2. Loans (long term) It

is assumed that i'L(t) is discreet, i.e. that i'L(t) = 0 and i'D(t) = 0 (171) for

all t > 0, apart from certain selected times tq where, in

practice, chan-ges take place in financing conditions, and new investments

are made. Subject to these assumptions equation (72) may be reduced to i'K(t) = i'B(t) (172) with

the condition i'L,D(t) = 0 In

close connection with the operational financial possibilities of equations

(171) and (172) this model also assumes that equation (173) applies: y'L(t) = r'L(t) (173) 12.3.3. Investments Investments

are defined by i'(t). It is here assumed that i'(t) = 0 apart from certain times tp corresponding to the forms of investment seen in

practice. In

this mathematical model equation (75) is changed into: i'(t) = i'L,i(t) (174) where

i'e(t)

thereafter becomes the quantity, cash flow released, for the following

purposes: - 44 - New investments Instalments on

loans Etc. This

change of equation (75) is desirable seen in relation to the possibili- ties

of implementing this mathematical model on a computer. 12.4.1. Interest payments From

equations (78), (79), (80), (170) and (173) the total interest payment is

derived: y'B(t) + y'L(t) = rB B(t) + rL L(t) (175) where

rB is interest rate bank and rL is interest rate lender. 12.4.2.

Depreciation Depreciation

to tax computation is obtained from equation (77) and is expressed as: d'2(t) = aD D(t) (176) where aD is the depreciation rate per time period. 12.4.3. Tax payments From

equations (81), (175) and (176) the following equation is derived: f'u(t) = aD D(t) + rB B(t) + rL L(t) (177) By

using equations (82) and (177) total tax payments are expressed as: H'S,1(t) = s(O'DS(t) - aD D(t) - (rB B(t) + rL L(t)))

(178) - 45 - 12.4.4. Cashflow released With

the special definition of i'e(t) given in 12.3.3. cash flow released is defined

by: i'e(t) = O'(t) - H'S,1(t) - (y'B(t) + y'L(t)) which

together with equation (88) gives: i'e(t) = l'(t) + dK(t)/dt - H'S,1(t) - (y'B(t) + y'L(t)) If

equation (168a) including the related assumption is used here, the follow-

ing equation is obtained: i'e(t) = l'(t) - H'S,1(t) - (y'B(t) + y'L(t)) + i'B(t)

(179) or

if equations (175) and (178) are used: i'e(t) = l'(t) + i'B(t) - s O'DS(t) + s aD D(t) - (1 -

s)(rB B(t) + rL L(t)) (180) By

using equations (62) and (87), the following equation is derived from

equation (180): i'e(t) = O'(t) - s O'DS(t) + s aD D(t) - (1 -

s)(rB B(t) + rL L(t)) (181) If

the function O'L(t) is defined by the equation: O'L(t) = O'(t) - s O'DS(t) (182) O'L(t) may be designated as the profit after tax from the

operating system. Equation

(181) is now transformed into: i'e(t) = O'L(t)(1 + s aD D(t)/O'L(t) - (1 -

s)(rB B(t) + rL L(t))/O'L(t) (183) It

appears from equation (183) that it may be appropriate to define the fol-

lowing managerial ratios: - 46 - 12.4.4.1. Interest relative Interest

relative is defined by equation (183): rB B(t) + rL L(t) rrel = - (1 - s) ¾¾¾¾¾¾¾¾¾¾¾¾ (184)

O'L(t) rrel can be interpreted as interest payments after tax

in relation to profit after tax from the operating system. 11.4.4.2.

Depreciation relative Depreciation

relative is defined by equation (183): aD D(t) arel

= s ¾¾¾¾¾¾¾ (185)

O'L(t) arel may be interpreted as the improvement in cash flows

after tax as a result of depreciation in relation to profit after tax from

the operating system. - 47 - 13.1. Traditional ratios In

this Chapter some traditional ratios will be computed on the basis of the

functional expressions derived in section 12. 13.1.1. Contribution ratio The

contribution ratio DG(t) is defined by the following equation (186): S'u,1(t) - (U'd,1,1(t) - F'i,2(t)) DG(t) = ¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾¾

(186) S'u,1(t) or

by using equations (49), (30), (22) and (23): O'(t) + F'b DG(t) = ¾¾¾¾¾¾¾¾¾ (187) S'u,1(t) 13.1.2. Profit ratio The

profit ratio is defined by the following equation (188): O'(t) OG(t) = ¾¾¾¾¾¾ (188) S'u,1(t) 13.1.3. Break-even sales Break-even

sales are defined by equation (189): F'b NS'(t) = ¾¾¾¾¾

(189)

DG(t) i.e.

the amount of sales where fixed costs are just covered by sales. - 48 - 13.1.4. Margin of safety The

margin of safety is defined by equation (190): S'u,1(t) - NS'(t) SM(t) = ¾¾¾¾¾¾¾¾¾¾¾ (190)

S'u,1(t) 13.1.5. Applications, examples It

appears from the above definition equations (187),(188), (189) and (190) that

they reflect general financial states in the model Fig. 2.1. Thus,

the contribution ratio DG(t) provides a good measure of the characteri- stics

of the change in liquidity l'(t) at a given turnover, i.e. i'(t) = DG(t) S'u,1(t) - F'b (191) this

approximation being achieved by using equations (187) and (87). The

profit ratio OG(t) enables the same possibilities of analysis as the con-

tribution ratio (compare equations (187) and (188)). It should be remembered,

however, that DG(t) is constant in time. The

profit ratio will be analysed in more detail in connection with the Dupont

Pyramid. For

the purpose of assessing the amount of sales in relation to a minimum le-

vel, two rough measures are available, the margin of safety and break-even

sales. It is important to bear in mind that these ratios are partial and nar-

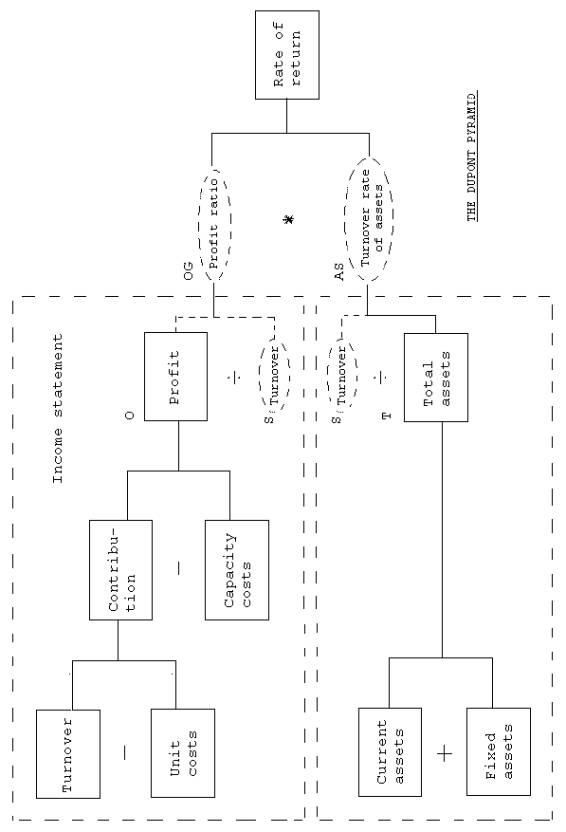

rowly defined for operations research purposes. - 49 - 13.2. Dupont pyramid Fig.

13.1. shows the Dupont pyramid containing the ratio, rate of return A. It will be seen that the Dupont

pyramid consists of two major components: Income Statement and Assets on the

basis of which the rate of return A by definition is computed as: O A = ¾¾¾ (192) T Equation

(192) can be transformed into O S A = ¾¾¾ ¾¾¾ (193) S T With

the definitions profit ratio OG and the turnover rate of assets AS, which are

both mathematical functions for operations research purposes, equation (193)

is given the form: A

= OG AS (194) In

connection with the computation of total assets T it is essential to note

that for accounting purposes it is difficult to determine the exact value of

the assets. How is, for example, the value of production machinery to be

valu- ed? The rate of return defined by equation (192) is thus a rough

measure of the financial efficiency of the production facilities. It

is pointed out that equation (194) has the same resulting informative con-

tents as equation (192). In equation (194) an extra variable in the form of

sales S has been put in. This ratio technique, which has been adopted by,

among others, Bela Gold, will be considered in greater detail in the follow-

ing pages. - 50 –

Figure 13.1 The

Dupont Pyramid - 51 - 13.2.1. Ratio mathematics, general For

the ratio U given by equation (195): y U = ¾¾¾ (195) x where

y and x are system variable and/or system state functions, financial or

physical, the general function given by equation (196) applies in the same

system:

y x1 xn xn+1

U = ¾¾¾

( ¾¾¾ - - - - ¾¾¾) ¾¾¾ (196) x1 x2 xn+1 x In

equation (196) xi for i = 1, -

- - -, n is an arbitrary quantity of system variable and/or system state

functions. If

we define the ratio G1

= y/x1, Gi = xi/xi+1 for i = 1, - - - , n and Gn = xn+1/x,

equation (196) may be given the equivalent form: U = G1 G2 G3 - - - - Gn (197) This

is exactly the ratio technique forming the basis of the computation of the

rate of return by the methods described in Section 12.2. (By the inserted va-

riable S in equation (193) or by the product method in equation (194)). A

look at Bela Gold's work on managerial ratios will show that equations (195),

(196) and (197) constitute the theoretical contents of Bela Gold's application

of ratios. It will be seen - 52 - that

exactly the assumptions underlying equation (196) are the reason why the

equation is not unique for a given system as regards the effect of the indi-

vidual ratios on U. Thus, these effects can only provide certain indications

as to states in the system under study. As

a result of the above comments on the lack of uniqueness of a number of

factors in a given development of a ratio, S, OG and AS are encircled by a

broken line in Fig. 13.1. The

above equations provide the theoretical background of the uncertainty found

in the literature on depiction of the Dupont pyramid. Thus, this pyramid is

often shown without the S, OG and AS areas encircled by broken lines. The

Dupont pyramid has a very simple memo-technical structure. This structure

consists of

Income Statment Assets Rate of return (ROI) The

Dupont pyramid is a kind of rough aid for analysis purposes rather than a

basic scientific figure with fundamental contents, cf. above. - 53 - Conclusion This

model of a company based on common accounting practrice presents all the most

applied functions of time giving management a picture of fundamental

characteristics in the company within accountancy, managerial economics, cash

flow, finance and physical resources. The business input parameters are di-

rectly available in the accountancy of the company. For

assessments of the soundness of cash flow released, two ratios have been

developed, interest relative and depreciation relative. The theoretical pro-

blem of Samuel Eilon,4-5 as

described in the introduction has been solved com- pletely. The

mathematical basis of Bela Gold's empirically applied ratio technique,7

has been discovered in order also to determine all the components in the

Dupont Pyramide as functions of time. As

a speciel powerfull result for management one may take the partial deriva-

tives of the funktions with the respect to the input data of accountancy and

also make the total differentials in order to make high efficient “what - if”

analysis. This implies also analysis of the effects of price elesticity of

markets. All

the functional expressions are implemented into the computer program MASI

proven in practice in more than 700 licensed installations in Scandinavia to

let the user get quick and deap insight into the dynamics of the company for

tactical and strategical planning purposes. The reader of this article may

ask for a licence to an english version under DOS, OS2 or WIN95 including a

manual (127 pages). - 54 - Acknowledgement Assosociate

Professor Mads Peter Soerensen, Department of Mathematical Model- ling, The

Technical University of Denmark, DK-2800 Lyngby, Denmark and profes- sor Jan

Mouritsen, Operation Management, Copenhagen Business School, Howitzvej 60,

DK-2000 Frederiksberg are gratefully acknowledged for illuminating

dis-cussions during the preparation of this manuscript. - 55

- BIBLIOGRAPHY

1. Ahlmark, Dan: Produkt - investering -

finansiering Ett bidrag till en teori foer foeretaget som ett produktcen- trerat finansiellt system. (292p) Handelshoegskolan i Stockholm Ekonomiska Forskningsinstitutet,

1974

2. Danielsson, Albert: Foeretagsekonomi. Begreppsbildning

och terminologie (79p) Studentlitteratur, Lund 1976 3. Danielsson,

Albert: Foeretagsekonomi

- en oeversikt (327p) Studentlitteratur, Lund 1975 4. Eilon,

Samuel & Cosmetatos, G.P.: A profitability model for tactical planning

OMEGA, Vol. 5, No. 6, pp673-688, 1977 5. Eilon,

S., Gold Bela, and Soesan J.:

Applied productivity analysis for industry (151p)

Pergamon Press, Oxford 1976 6. Forrester, Jay W.: Industrial

Dynamics (464p)

Cambridge, Mass.,M.I.T. Press 1977 7. Gold,

Bela:

Technological change. Economics, management and

environment (175p)

Pergamon Press, Oxford 1975 8.

Malmborg, Charles J.: Expected part delays as a secondary layout

criterion in

automated manufacturing systems App.

Math. Modelling 1997, 21: 301 - 313

Elsevier Science Inc. 1997 9.

Rappaport, Alfred:

Creating Shareholder Value (320p) Free

Press, Herts 1998 10. Segall,

R.S.:

Mathematical modelling of spatial price equilibrium for

multi commodity consumer flows of large markets

using variational inequalities App.

Math. Modelling, 1995, Vol 19, February

Elsevier Science Inc. 1995 |

|

|